The Group is devoted to producing automobile and motorcycle component parts. Downstream in the motorcycle industry refers to the assembled and ready-for-sale motorcycles. The midstream products include engines, power station system, steering system, brake system, tires and wheels system. Upstream is primarily the manufacturing of the components in the midstream products. Eurocharm Group is a midstream manufacturer in the automobile body and chassis system and in the medical equipment industry, selling products to brand customers.

Development Status of the Global Automobile Industry

In 2023, the global automobile market is expected to show signs of recovery. With the easing of the global chip shortage and the revival of economic activities as the pandemic subsides, it is beneficial to the performance of top countries in sales such as China, the United States, and Japan. In the wake of the ongoing Russia-Ukraine conflict, automobile manufacturers have partially shifted production capacities (such as wiring harnesses) from Russia and Ukraine to other countries. This may also prompt manufacturers to redesign future electric vehicles (such as wiring harnesses), thereby accelerating the phase-out of their petrol vehicles. The sales performance of the automobile market will be affected by the pace at which the chip shortage eases, the duration of the US-China trade war, and the accelerated adoption of electric vehicle driven by the net-zero carbon trend.

Looking at the global market trend for electric vehicles in 2023, Battery Electric Vehicles (BEVs) are a key focus for manufacturers due to their batteries as a 100% power source, enabling high energy efficiency, long duration, and fast charging technology. BEVs continue to increase their market share compared to Hybrid Electric Vehicles (HEVs), driven by policy incentives in various countries. While Hybrid Electric Vehicles (HEVs) currently remain competitive in terms of cost-effectiveness and user familiarity, their sales growth rate is slowing down as countries are providing more incentives for BEVs and Plug-in Hybrid Electric Vehicles (PHEVs). However, HEVs still play a significant role in supporting sales volume. PHEVs, which can recharge their lithium batteries by plugging in, are gradually losing growth momentum in their main market, China, as the country focuses more on pure electric vehicles. However, PHEVs, with their ability to switch to fuel operation when the battery is depleted, remain competitive in the absence of widespread charging infrastructure, with potential for a growing market share. Sales of fuel cell vehicle remain stable with potential applications in the commercial vehicle sector, and sales records have been solid in ten countries. Looking ahead, with the extension of battery duration, increased density of charging infrastructure, maturation of fast charging technology, and electric vehicle prices approaching market expectations, along with factors such as carbon reduction goals in various countries, strategic planning of manufacturers, and the easing of chip shortage, the global electric vehicle market is estimated to grow by 28.18% in 2023, reaching a scale of 20.16 million vehicles.

Global Industry of Motorcycles

The size of global motorcycle market in 2022 was 58,712 million units, with Asia being the largest market in the world, including India, mainland China, Indonesia, Vietnam, the Philippines, and Thailand, each with annual sales exceeding one million units. Taiwan and Japan had a combined sales volume of 1.096 million units. The Chinese market increased by 6.1%, and Japanese markets decreased by 4.5% in 2022, while the major Southeast Asian markets (Indonesia, the Philippines, Thailand, Vietnam, and Malaysia) grew by 10.6%. In 2022, Asia accounted for 87.3% of the global motorcycle market.

Analyzing the annual sales trends in each major region, Latin America grew by 3.6%, while other regions decreased by 11.9%. In 2022, Latin America accounted for 9.1% of the global market; other regions accounted for 0.5%.

North America market grew by 11.6% in 2022, and Europe (including only France, Germany, Italy, Spain, the United Kingdom, Belgium, the Netherlands) decreased slightly by 0.3%. In 2022, North America accounted for 1.1% of the global market, and Europe (France, Germany, Italy, Spain, the United Kingdom, Belgium, and the Netherlands) accounted for 2.1%.

In 2022, as the pandemic eased, outdoor activities increased, leading to a resurgence of interest in the motorcycle market. However, due to international turmoil, increasing raw material costs, and the effects on electric motorcycle products caused by the chip shortage, prompting some manufacturers to stock up early. A few manufacturers responded to the cost increase by raising prices, and consumers returned to rational purchases. The market in China was affected by zero-COVID policies. Meanwhile, the markets in Southeast Asia and India continued to recover in the post-pandemic era. The global motorcycle market in 2022 totaled 58.71 million vehicles.

The global motorcycle market continued to gradually improve in 2023, returning to the volume before the pandemic. In China, the end of the buffer period before the implementation of the new national targets, coupled with the gradual relaxation of zero-COVID policies, motorcycle sales figure was boosted. The main sales drivers in 2023 are expected to come from China, India, and Latin America, with the size of the global motorcycle market estimated at 60.99 million vehicles.

In 2021, the International Energy Agency (IEA) released a special report on the “Net-Zero Emissions Roadmap for the Global Energy Sector to 2050”, which suggested that countries should stop selling internal combustion engine vehicles by 2035. Japan and California of the United States announced the target of banning the sale of fuel vehicles in 2035. The Japanese government officially announced that it will achieve net zero emissions of greenhouse gases by 2050. France and Spain are expected to complete the ban on sales by 2040. In 2021, the Ministry of Renewable Energy of Indonesia proposed a plan to sell all-electric two-wheelers in 2040, and only sell electric vehicles nationwide in 2050. The Ministry of Renewable Energy of India has invested INR$950 million since 2011 to subsidize locally made electric vehicles, and even consider banning the sale of 150cc fuel motorcycles from 2025. European countries such as the United Kingdom have announced that they will stop the sale of fuel vehicles as early as 2030. France plans to completely stop the sale of gasoline and diesel vehicles from 2040. Germany, Belgium, Denmark, the United Kingdom, and India will completely ban the sale of new fuel vehicles in 2030. Asian motorcycles major country, Vietnam has also stipulated that fuel vehicles will be banned from entering Hanoi in 2030. Under the premise that advanced countries such as the European Union, the United States, and Japan have committed to net-zero transformation, the wave of electrification is imperative, and global fuel vehicle manufacturers are also striving for transformation to seize the key markets of the next generation. Electric motorcycles and traditional motorcycles have many common components, including body, steering, braking and shock absorber systems. The company mainly produces aluminum parts, stamping parts, welding parts and related locomotive metal parts, which can be shared with electric motorcycles.

Motorcycle Trends in Vietnam

Due to factors such as Vietnam’s underdeveloped public transportation institutions, high car prices compared to income levels, and the ability to drive electric motorcycles with a displacement of 50cc or less without a license, traditional motorcycles remain a widely common mode of transportation. As a result, the market has reached the saturation point. Vietnam is the fourth largest motorcycle market in the world. The Vietnamese motorcycle industry is mainly comprised of five major companies, including Honda, Piaggio, Suzuki, SYM, and Yamaha. Despite the severe impact of the COVID-19 pandemic, motorcycle sales increased by 29%, indicating that these products are still attractive in the market. In addition, Vietnam has stipulated that the sale of fuel motorcycles will be banned in 2030, with the goal of reducing carbon dioxide emissions by 8% by 2030. According to estimates by Hanoi University, Vietnam’s electric motorcycles account for only 1.5-1.8% of Vietnam’s total motorcycles sales. In the future, problems such as improving charging infrastructure need to be solved.

Medical Equipment Market

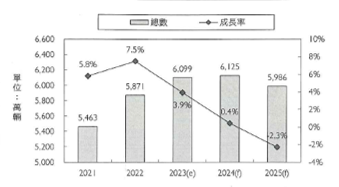

The Company’s medical equipment products, including lifting hangers for patients, bath chairs, commode chairs, and medical beds, is mainly sold in Japan, Europe, and North America. According to the statistics by BMI in 2022, the global medical equipment market size in 2021 is US$483.27 billion, an increase of 6.4% over 2021. It is estimated that it will reach US$589.68 billion in 2025, with a compound annual growth rate of about 6.7% from 2021 to 2025.

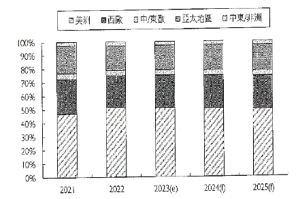

In 2022, the medical equipment market is still dominated by the Americas, accounting for 51.7% of the global market. The second largest market was Western Europe, accounting for 23.5%, followed by Asia-Pacific region, which accounted for 18.2% of the global market. Central and Eastern Europe accounted for 3.8%. The Middle East and Africa accounted for 2.8%. It is expected that the overall ranking of the regional markets in the future will not change much. The Americas, Western Europe, and Asia-Pacific regions are still the top three markets, but the proportion varies slightly among them.

The major markets in the Americas include the United States, Canada, Mexico, and South America countries. In 2022, the market in the Americas accounted for 51.7%, The size of the American market is 249.69 billion, an increase of 17.6% from 2021, with an estimated compound annual growth rate of 8.4% from 2021 to 2025. With strong US dollars, the market size has gained more growth compared to that in 2021. The US market has accounted for about 90% of the American market over the years, serving as the main growth driver in the Americas. Due to factors such as the aging of the baby boomer generation and the continued decline in birth rate, population of the aged 65 and above continues to rise, reaching 17.1% in 2022. In addition, chronic diseases have been increasingly prevalent over the years, leading to the continuous growth of overall healthcare spending in the United States. Furthermore, the COVID-19 pandemic also increased healthcare demand. Total healthcare spending in the U.S. reached $4.7 trillion in 2022, a 11.2% increase from 2021, and overall healthcare spending accounted for 18.4% of the GDP. In 2022, the average healthcare expenditure in the United States reached US$13,874.1, representing a 9.5% growth from 2021. Both healthcare expenditures and their proportion to GDP are the highest in the world.

In 2022, the healthcare market in the Americas experienced a post-pandemic recovery, showing overall rapid market growth. On the other hand, negative factors included the financial difficulties faced by many hospitals post-pandemic, as well as a wave of healthcare worker resignations due to prolonged pandemic stress. In March 2022, the US Department of Health and Human Services announced it would provide an additional $4.13 billion in relief funds from the Provider Relief Fund (PRF) to over 3,600 healthcare service providers affected during the pandemic. This funding covers costs related to Covid-19 testing, diagnosis, treatment, and vaccines, aimed at compensating smaller healthcare facilities that suffered greater losses during the pandemic. This relief effort, the fourth round since it began in November 2021, has disbursed a total of $13.5 billion, benefiting approximately 86,000 facilities. Additionally, the Health Resources & Services Administration (HRSA) has distributed nearly $7.5 billion to over 44,000 healthcare facilities across the US through the American Rescue Plan rural payments, which will help recruit or retain healthcare workers, enabling them to continue operations and care for patients. These policies aim to maintain the stability of the healthcare system, as the enormous healthcare demand in the US will continue to be a key driving force for the growth of the healthcare equipment market in the Americas.

The Western European region remains the world’s second-largest market. In terms of market size, countries include Germany, France, the United Kingdom, Italy, Spain, the Netherlands, Switzerland, Belgium, Austria, Sweden, Denmark, Norway, Ireland, Finland, Portugal, and Greece, among others. The top four countries have consistently been among the world’s top 10 single-country medical equipment markets, accounting for approximately two-thirds of the Western European market. In 2022, the Western European market was valued at $113.59 billion, a decrease of 2.5% from 2021. The compound annual growth rate from 2021 to 2025 is estimated to be 5.4%. The Western European market accounted for 23.5% of the global market in 2022, a slight decrease from 25.7% in 2021. The main factors contributing to this decrease were the significant depreciation of Euro and Pound in 2022. When priced in Euro, the Western European medical equipment market grew by 9.4% compared to 2021. This growth was driven by the significant demand for healthcare equipment in Europe due to its aging population and the rebound in demand for medical materials as pandemic restrictions eased. Western Europe has the highest level of aging population in the world, with over 85 million elderly people. Many Western European countries have already entered an aged society where the proportion of elderly people exceeds 14%. In 2022, the Netherlands joined Italy, Finland, Portugal, Greece, Germany, France, Denmark, and Sweden as the ninth Western European country to enter the “super-aged society” with an over 20% elderly population. The aging population has led to an increase in the prevalence of chronic diseases, driving continuous growth in demand for medical care products. Additionally, as vaccination rates increase and the pandemic subsides in European countries, various medical measures are gradually returning to normal, leading to a more active Western European medical equipment market. In response to the long-term medical needs of an aging society. The “Innovative MEDICAL devices of Tomorrow” initiative of France has included medical device innovation as a strategic blueprint item for 2030, allocating €400 million to accelerate innovation and commercialization in areas such as in-vitro diagnosis, surgical robotics, implants, prosthetics, and digital healthcare, aiming to make France a leading European country in medical innovation. These favorable policy factors are expected to be key drivers of growth in the European medical equipment market.

In 2022, the Asia-Pacific medical equipment market was valued at $88.1 billion, accounting for 18.2% of the global market. Due to the depreciation of exchange rates against the US dollar, this share decreased slightly from 20.5% in 2021. The market size decreased by 5.5% compared to 2021. The compound annual growth rate from 2021 to 2025 is estimated to be 5.1%. The medical equipment market in the Asia-Pacific region is primarily driven by China and Japan, which accounted for 36.1% and 26.9% of the Asia-Pacific market in 2022, respectively. The combined share of China and Japan in the Asia-Pacific market has consistently been over 60% in recent years. South Korea, Australia, and India each accounted for between 10% and 5%. Other countries in the Asia-Pacific region accounted for less than 5% each. Among the ASEAN countries, Malaysia has the largest share of the medical market at around 2%, while Thailand, Vietnam, Indonesia, and Singapore each account for less than 2% of the Asia-Pacific market. In sum, the development of the Asia-Pacific medical equipment market is mainly driven by China and Japan.

In 2022, the top ten single markets for medical equipment globally were the United States, Germany, China, Japan, France, the United Kingdom, Italy, Canada, South Korea, and Spain. Compared to the ranking in 2021, South Korea has risen from the 10th to 9th place, while Spain has replaced the Netherlands in the 10th place.

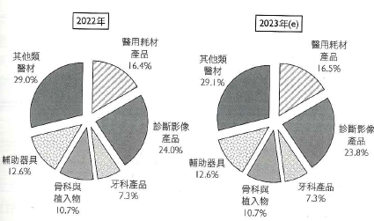

In terms of product sales by category, “other medical equipment” took the highest proportion in 2022, accounting for 29% of the market share, which is a slight increase from 27.8% in 2021. This category includes products such as electric and manual wheelchairs, dialysis equipment, endoscopy equipment, anesthesia equipment, blood pressure monitoring products, medical furniture, and ophthalmic equipment. As these products are developed in response to various diseases and essential for treatment, they are part of the basic equipment and consumables in hospital. Due to the impact of the pandemic, many hospitals have postponed the replacement and upgrading of their basic equipment. It was not until 2022, as the economy gradually returned to normal, that the rebound in demand drove sales growth. As the product market was originally relatively large, its share also increased accordingly.

The largest single category is the diagnostic imaging products, accounting for about 24.0%, an increase of 0.4% compared with 23.9% in 2021. Medical consumables accounted for 16.4%, a slight decrease of 0.1% compared to 2021. Such products are proportional to the number of people who need medical care. The COVID-19 pandemic drove the need for essential medical consumables, resulting in a rapid growth of the medical consumables market that brought a higher market baseline. On the other hand, assistive devices accounted for 12.6%, a decrease of 0.3% from 13.0% in 2021; dental products accounted for about 7.3%, a decrease of 0.1% compared to 2021. Orthopedics and implants products accounted for about 10.7%, a decrease of 0.8% compared with the 11.5% in 2021. Orthopedic and dental products are often considered deferrable medical procedures. During the COVID-19 pandemic, healthcare facilities postponed non-urgent medical procedures, resulting in delays for non-urgent surgeries and treatments. Additionally, due to concerns about infection, people voluntarily reduced non-essential healthcare visits, such as non-life-threatening dental treatments or procedures, affecting the growth of these two categories of products, which already had smaller market sizes. After the pandemic eased in 2021, there was a rebound in demand for dental and orthopedic care, with a higher growth rate and a higher base. In 2022, although demand remained strong, the dental equipment market was hampered by generally poor economic conditions, leading to a slowdown in its growth. The orthopedic market was affected by a wave of healthcare worker resignations and the bulk purchasing policy in mainland China, which lowered product prices, resulting in slower market growth compared to 2021.

Product Trends

Automobile Industry

In the next 10 years, the global automobile industry will face the most significant change in history, with electric vehicles replacing internal combustion engine vehicles. The overall automobile market was underperforming due to chip shortages, while the electric vehicle market is showing substantial growth.

DIGITIMES Research predicts that the penetration rate of the electric vehicle market will exceed 30% in 2025, and the compound annual growth rate of electric vehicles will exceed 50% from 2020 to 2025. The development trend of the electric vehicle industry is towards four directions, including flattening of supply chain, a more friendly price, popularization of charging stations, and intelligent electric vehicle design.

The number of components required for pure electric vehicles is estimated to be 30% to 40% less than internal combustion engine vehicles, and the manufacturing process is more simplified and involves fewer suppliers. Therefore, the supply chain is less stratified, and the winner of the supplier should have more bargaining power than the small original equipment manufacturer. In the short term, the price of batteries and traction motors may continue to drive up electric vehicles manufacturing costs. The profit margin of pure electric vehicles for original equipment manufacturer is probably not as profitable as for electric vehicles battery makers and their suppliers of specific components.

In the mid- to long-term, with market concerns over electric vehicles performance (such as battery durability, driving experience and platform construction) receding, future growth will be driven by incentives, regulations, subsidies, local advantages, and customer preferences. Likely winners will include electric vehicles suppliers focusing on specific component. These auto suppliers have established scales in key areas and increased bargaining power. The original equipment manufacturers who can successfully transform between internal combustion engine vehicles and new energy vehicles (including electric vehicles) and acquire a balanced status, and those new entrants that can scale up quickly are also possible winners. Investors need to be mindful of these factors to identify emerging winners and losers and actively reposition their portfolios to grasp on investment opportunities.

Motorcycle Industry

As global warming and air pollution continue to simmer, automotive manufacturers are launching environmentally friendly products to help preserve the planet. With the current research and development towards advanced technology, automotive manufacturers are exchanging ideas with their long-term suppliers who are the parts manufacturers. This is beneficial to both the upstream and midstream companies as they can apply newly developed technologies to manufacture higher quality products and, at the same time, reduce the processing waste to ease off the pollution.

In addition, with the rise of electric motorcycles in developed countries and the rapid economic growth in Southeast Asian countries, the demand for motorcycles has been increasing annually. Major Japanese motorcycle manufacturers, such as Honda, Yamaha, Piaggio, and Suzuki, have gradually shifted their focus to ASEAN countries in pursuit of related business opportunities. They utilize low-cost local labors and procure competitive components and then assemble and sell their products locally. Countries such as Indonesia, Vietnam, and Thailand, which have experienced significant growth in the motorcycle market, have become targets for competitors in the industry. Eurocharm Group has not only become a major supplier in the Vietnamese market but is also actively exploring the potential of other ASEAN Plus Five Trade Area. The Company is adjusting its priority of sales from Vietnam to international markets. Furthermore, following such strategies, the Company has invested in new manufacturing processes and precision equipment to enhance product quality and streamline the production procedure to acquire the competitive advantage for future market development.

Medical Equipment Industry

COVID-19 has rapidly impacted all parts of the world, and the structure of medical demand has greatly affected the medical equipment industry. New demand and the introduction of new technologies have also accelerated the transformation of the industry. At the same time, the global aging population continues to drive up the demand for medical care. Countries are actively seeking more efficient medical solutions, promoting relevant technology and policy in fields such as precision health and digital medicine, hoping to accelerate the development of advanced medical technology to achieve improved medical care. In response to the clinical application of emerging technologies such as artificial intelligence and digital technology, governments around the world have also begun to revise relevant medical device regulations to ensure the product safety while accelerating the public’s access to advanced medical technology. Through cross-disciplinary integration and cooperation with physicians, medical device manufacturers innovate products and solutions that meet clinical needs and expand new opportunities for the medical industry. According to the study report from BMI Research, the market size of the global medical equipment reached US$483.27 billion in 2022, which was a 6.4% of growth compared to that in 2021. It is estimated that the market will expand to US$589.68 billion in 2025. The compound growth rate between 2021 to 2025 is about 6.7%.

Competition

VPIC1, the sub-subsidiary of the Company, was established in Vinh Phuc Province, Vietnam in 2001. Its major business is manufacturing of motorcycle parts. There are two major domestic competitors, Cosmos Industrial Co., Ltd and Kyoei Manufacturing Co., Ltd. Established in 2005, Cosmos produces metal components in the same province. Kyoei, headquartered in Japan, manufactures motorcycle and recreational chassis locally in Vietnam.

As for the medical equipment market, Eurocharm’s primary competition is Li Wei Co., Ltd., which manufactures medical beds as well as hangers, rails, and tables for medical beds, rails. Founded in 1994, Li Wei operates facilities in both Taiwan and China.