Climate Change Adaptation

On November 12, 2021, the Glasgow Climate Pact was formulated during the COP26 climate conference. This marked the first clear declaration to reduce the use of coal and pledge increased funding to help developing countries adapt to climate change. The goal is to limit the temperature rise to 1.5 degrees Celsius, aligning with the global climate target set in the Paris Climate Agreement. Governments are urged to propose carbon reduction schedules and positive paths. In 2015, the Financial Stability Board established the Task Force on Climate-related Financial Disclosures (TCFD) work group. Its mission is to develop a unified set of recommendations for voluntary disclosure on climate-related finance. This initiative aims to help investors and decision-makers better understand the significant risks faced by businesses and to assess climate risks and opportunities more accurately. The Group follows the framework of the TCFD for disclosing climate-related information, which includes four main categories: governance, strategy, risk management, as well as metrics and targets.

Governance

Board of Directors’ Supervision on Climate Risks and Opportunities

The Company established the Sustainability Management Committee and the Risk Committee in June 2022. The Sustainability Management Committee is responsible for formulating sustainability policies, systems, or relevant management guidelines, as well as implementation plans. Meetings are held at least quarterly to report to the Sustainability Management Committee on the implementation status and the tracking, reviews, and revisions of the results. The Risk Committee is responsible for reviewing risk management policies, risk management frameworks, major risk management strategies, and management reports on major risk issues, as well as supervising improvement mechanisms. It regularly reports on the implementation of risk management to the Board of Directors.

Climate change is included in risk topics, and at least two meetings are held annually for reporting to the Risk Management Committee. The Board of Directors is responsible for approving sustainability policies, systems, or relevant management guidelines and specific implementation plans. It also approves risk management policies, procedures, and frameworks to ensure the alignment of operational strategies with risk management policies. The committee establishes appropriate risk management mechanisms and risk management culture, supervises as well as ensures the effective operation of the overall risk management mechanism, and allocates and assigns ample and appropriate resources to ensure effective risk management operation.

The Role of the Management Level in Assessing and Managing Climate Risks and Opportunities

The audit office is responsible for promoting and implementing risk management policies and reviewing the implementation of risk management in various departments of the Company in accordance with current laws and regulations The executive meetings or operational meetings chaired by the general managers of each subsidiary are responsible for overseeing and reviewing the implementation status of the Company’s risk management, risk assessment, and risk acceptance. Managers of the business units are responsible for frontline risk management, including identifying, analyzing, monitoring, measuring, and responding to relevant risks within their units to ensure that risk control mechanisms and procedures are effectively implemented.

Strategies

Short-term, Mid-term, Long-term Climate-related Risks and Opportunities Identified

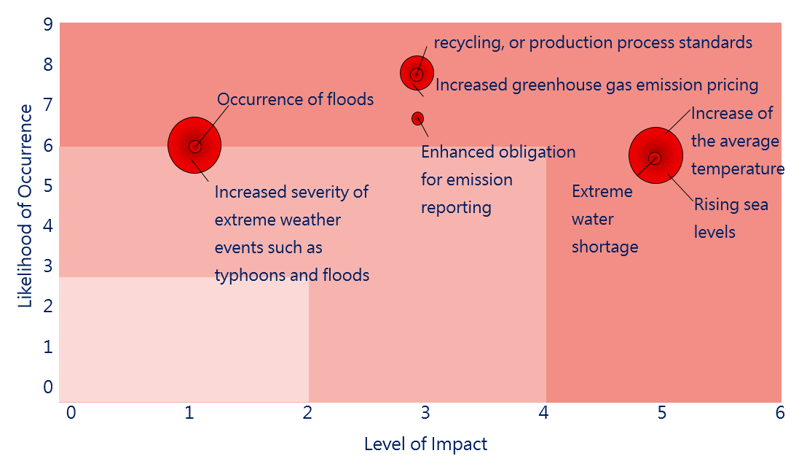

The General Administration Office is responsible for identifying climate risks and opportunities, assessing them based on three main aspects: Potential Impact, Potential Vulnerability, and Likelihood. Likelihood is further categorized as follows: Certain (>99% likelihood), Almost Certain (>90% likelihood), Likely (>66% likelihood), Possible (>50% likelihood), Moderately Possible (33-50% likelihood), Unlikely (<33% likelihood), Very Unlikely (<10% likelihood), and Impossible (<5% likelihood). Time of occurrence is categorized into Long-term (in more than 5 years), Mid-term (in 1 to 5 years), and Short-term (in less than a year). Severity is categorized into Catastrophic, Severe, Major, Moderate, and Minor. By creating a Climate Risk Matrix, we have completed the management and mitigation strategies for climate risks. The Climate Risk Matrix enables our company to better understand the impact of climate change on our business and guides us in responding to and managing risks in the future. Please refer to the 2023 Climate Change Risk and Opportunity Matrix for further details.

Climate-related Risks and Opportunities of the Organization’s Business, Strategies, and Financial Planning

Based on the climate-related risks and opportunities specified by TCFD as well as learning from benchmark companies, 141 climate-related risks and opportunities were identified. These were further narrowed down to 9 climate risks and 5 climate opportunities for in-depth climate scenario analysis. The management of climate-related risks and opportunities has been integrated into the Company’s management processes. Please refer to the impacts of climate change risks and opportunities on our strategies, operations, and financial planning.

Strategic Resilience of the Organization, Considering Scenarios under Different Climate (Including at 2˚C or under more Severe Conditions)

Climate Scenario Analysis

The Company, following the TCFD framework, analyzes certain transition and physical risks to assess the potential impact on our operations or supply chain under different scenarios of the global greenhouse gas emission control. The results are incorporated into our considerations for strategic resilience. The Company refers to the International Energy Agency (IEA) and the Intergovernmental Panel on Climate Change (IPCC), the two organizations responsible for compiling global scientific findings related to climate change. These organizations publish assessment reports every 5 to 7 years, providing updates on scientific progress on climate change, which serve as references for decision-making and academic research. Due to the high uncertainty of future climate change, previous analyses were conducted using the worst-case scenario. This time, we have adopted multiple scenarios to evaluate our internal operational strategy planning and communication, providing a more comprehensive understanding of mid- to long-term climate development trends.

Choosing Climate Scenarios

As countries have reached a consensus on viewing the Carbon Pricing Scheme as a necessary policy to achieve net zero emissions, our company, in assessing transition risks, refers to the 2022 World Energy Outlook (WEO 2022) published by the IEA, which is widely used by international enterprises. We have selected the Stated Policies Scenario (STEPS), the Announced Pledges Scenario (APS), and the Net Zero Emissions by 2050 Scenario (NZE) to analyze future carbon pricing, serving as the basis for assessing the impact of carbon pricing schemes on our operational locations in different countries.

As for physical risks, IPCC has released the 6th Assessment Report (AR6) since 2021, using the latest Global Climate Models (GCM) to estimate long-term climate change, and adopting Shared Socioeconomic Pathways (SSP) to consider greenhouse gas emissions under different social and economic scenarios. A comprehensive assessment of climate change covering all regions of the world as well as Downscaling analysis has been provided. This offers a more detailed impact assessment for the operation locations of our group.

Descriptions of the Climate Scenarios

| Types of Risks | Scenarios Chosen | Scenarios Description | Key Parameters | Content of Evaluation |

|---|---|---|---|---|

| Transition Risks and Opportunities | IEA-STEPS (Stated Policies Scenario) IEA-APS (Announced Pledges Scenario) IEA-NZE (Net Zero Emissions by 2050 Scenario) | Development and potential challenges under stated policies: By 2100, the global average temperature is projected to rise by around 2.5°C compared to that prior to the industrial era. lThis scenario incorporates the latest climate commitments from various countries, including their Nationally Determined Contributions and long-term net-zero goals. Assuming these commitments are fulfilled as scheduled, the global average temperature is projected to rise by around 1.7°C compared to that during pre-industrial era by 2100. This scenario aims for achieving the global target of temperature rise by 1.5°C and widespread use of modern energy by 2030. | The assumed carbon pricing for operation locations or regions under different scenarios | Evaluating the corresponding carbon pricing trends and carbon regulatory laws for operation locations under scenarios targeting temperature control at 2.5°C, 1.7°C, and 1.5°C. Impacts of the possible expenses relevant to carbon emissions in 5 to 10 years. |

| Physical Risks | lIPCC-AR6 SSP1-2.6 Low Emission Pathway lIPCC-AR6 SSP5-8.5 High Emission Pathway | Given the possibility of a multi-model mean below 2°C by 2100, SSP1 was chosen for its significant land-use changes (increased global forest cover), representing a scenario with low vulnerability, low mitigation pressure, and low radiative forcing. lSSP5 is the only SSP scenario with emissions high enough to produce a radiative forcing of 8.5W/m2 by 2100. | Extreme climate causes changes in rising sea levels and the pressure of water shortage | Assessing the intensification of water scarcity and the increase in the number of severe typhoons due to extreme climate conditions in the highest warming scenario. Evaluating the operational impacts resulting from potential higher costs in alternative transportation and equipment maintenance during the mid-century. Assessing the risk changes in sea-level rise, impacts of sea level, flood, and water level, as well as pressures from water scarcity caused by extreme climate warming under scenarios of ideal mitigation or maximum warming. |

Risk Management

Identification and Evaluation Process of the Climate-related Risks and Opportunities

The Company, following the TCFD framework, identifies risks/opportunities that have impacts of business, strategies, and financial planning. Risks/opportunities are defined and listed by the General Management Office. Referencing the IPCC AR6’s SSP1-2.6 and SSP5-8.5 climate scenarios, the Company conducts risk assessments on transition risks, immediate physical risks, and long-term physical risks. This helps us identify and analyze short-, medium-, and long-term climate risks and opportunities within the Company’s scope.

Transition Risks

In the future, carbon pricing under different schemes (total greenhouse gas control, carbon taxes, carbon fees) and climate scenarios may vary greatly and have high uncertainty. Therefore, to ensure that the overall reduction strategy aligns with future policy and regulatory trends, the Company make assumptions on the current or future carbon pricing mechanisms at its operation locations and assesses the range of financial impacts that may occur. As of March 31, 2023, according to carbon pricing data published by the World Bank, the average price of the Emissions Trading System (ETS) for Europe is EUR 96.298125 per ton; the average price of ETS for Germany is EUR 32.625 per ton; the average price of the carbon taxes in Mexico is USD 3.721677955 per ton, and Taiwan has not yet implemented a carbon fee, but it is estimated to be NT$300 dollars per ton. Vietnam has not yet implemented carbon pricing.

Physical Risks

To accurately identify and measure the impact of climate change physical risks on operations, the Company references the IPCC AR6 SSP scenarios. We select the SSP1-2.6 low-emission pathway (i.e., temperature increasing by 1.8 °C by 2100) and the SSP5-8.5 high-emission pathway (i.e., temperature increasing by 4.4 °C by 2100) for physical risk analysis. We fully examine the short-, medium-, and long-term risks of sea-level rise, sea level and floods, and water level effects due to warming. The analysis indicates that both the Vietnam and Taiwan facilities are at low risk. Additionally, based on scenario assumptions, the Company regards the pressure of water scarcity for the Vietnam Khai Quang plant and the Taiwan plant as moderate to low risk before 2050 under the SSP1-2.6 (optimistic) and SSP5-8.5 (pessimistic) scenarios. The Bai-Shan plant in Vietnam is classified as high risk for pressure of water scarcity before 2050 under both scenarios.

Impacts on Strategies, Operations, and Financial Planning Resulting from Climate Change Risks

| Types | Climate-related Risks and Opportunities | Characteristic Description of the Impact on Eurocharm | Scope of Influence | Severity | Time of Occurrence | Scenario Description of the Financial Impact to Eurocharm |

|---|---|---|---|---|---|---|

| Transition | Increased greenhouse gas emissions pricing | The CBAM certificates have been implemented starting from October 1, 2023. Importers affected by this measure only need to declare the carbon emissions of their relevant products during the transitional period. From 2023 to 2025, there will be free quotas and no need to purchase CBAM certificates, therefore, there is no financial impact for now. Starting from 2026, the free quotas will be gradually reduced, and businesses will need to purchase CBAM certificates to make up for the gaps. As of December 31, 2023, the trading price of CBAM certificate is 80.19 Euros. On June 7, 2022, U.S. senators proposed the Clean Competition Act (CCA) to the Congress, aiming to reduce pollution and strengthen the competitiveness of U.S. manufacturing industry. The current price is set at US$55 per metric ton, with a 5% annual increase to account for inflation. | Upstream or our suppliers Company’s direct operation Downstream or our customers | Major | Mid-term | ● The CBAM certificates have been implemented starting from October 1, 2023. During the transition period, importers affected by this measure only need to declare the carbon emissions of their relevant products and do not need to purchase CBAM certificates yet. Therefore, there is no financial impact for now. ● The Company has obtained the Greenhouse Gas Assurance Statement for 2022 and introduced ISO 14067 in September 2023 to establish a model for calculating product carbon emissions to meet import and export declaration requirements and customer demands. The consulting fee was 130,000,000 Vietnamese Dong (approximately NT$170,000). ● In the future, carbon pricing under different schemes (total greenhouse gas control, carbon taxes, carbon fees) and climate scenarios may vary greatly and have high uncertainty. Therefore, to ensure that the overall reduction strategy aligns with future policy and regulatory trends, the Company make assumptions on the current or future carbon pricing mechanisms and assesses the range of financial impacts that may occur. As of March 31, 2023, according to carbon pricing data published by the World Bank, the average price of the ETS for Europe is EUR 96.298125 per ton; the average price of ETS for Germany is EUR 32.625 per ton; the average price of the carbon taxes in Mexico is USD 3.721677955 per ton, and Taiwan has not yet implemented a carbon fee, but it is estimated to be NT$300 per ton. Vietnam has not yet implemented carbon pricing. |

| Transition | Enhanced obligations for emissions reporting | Financial Supervisory Commission has released the Sustainable Development Roadmap for listed companies, setting a timetable for the disclosure of greenhouse gas inventory. The companies required to disclose such information are divided into four groups based on their paid-in capital. The content to be disclosed includes direct greenhouse gas emissions (Scope 1) and energy indirect emissions (Scope 2). The disclosure boundary must be consistent with the scope of the company’s consolidated financial statements. Eurocharm, a listed company with paid-in capital of less than NT$5 billion, is required to complete the inventory of the listed parent company by 2026, the inventory of subsidiaries included in the consolidated financial statements by 2027, the assurance of the listed parent company by 2028, and the assurance of subsidiaries by 2029. | Upstream or our suppliers The Company’s direct operation Downstream or our customers | Minor | Mid-term | ● Since September 2022, the group has introduced ISO 14064-1 for greenhouse gas inventory. Currently, we have completed greenhouse gas inventory and assurance for both parent company and subsidiaries, including Eurocharm Holdings, B.V.I, Eurocharm H.K., Eurocharm U.S., Eurocharm TW, and VPIC1. Internal audits are conducted annually, and assurance is provided by a third-party external organization. The assurance fee for these three years is NT$675 thousand. |

| Transition | Policies and Regulations | ● The National Development Council announced the “Taiwan 2050 Net-Zero Transition Goals and Actions” on December 28, 2022. The carbon reduction target for 2030 is set at 24% plus or minus 1%. The five major actions include strengthening the establishment of renewable energy, energy conservation, electrification of transportation, carbon sinks and negative emission technologies, as well as international cooperation on carbon reduction. Vietnam self-determined its contribution plans; By 2030, Vietnam aims to reduce its total greenhouse gas emissions by 9%, equivalent to 83.9 million tons of carbon dioxide. | The Company’s direct operation | Minor | Mid-term | ● From 2023 to 2025, the expenditure on the consulting of ISO 50001 energy management system and three-year verification for our factories in Taiwan and Vietnam amounted to NT$915,000. ● In 2023, Eurocharm TW replaced two sets of air conditioning at a cost of NT$100,000. Starting from July 2023, the equipment management department of VPIC1 Vietnam conducted inspections for gas leakage in various departments, identifying types of leaks, including fast joint leaks, gas pipe joint leaks, and electromagnetic valve leaks, with the number of leakage locations totaling 1,872 as of December 2023. Air control valves were installed for improvement. |

| Physical | Increased severity of extreme weather events such as typhoons and floods | ● Flooding or drought caused by long and intermittent heavy rain, leading to equipment failures in the factory area and resulting in premature demolishment of the assets. | The Company’s direct operation | Minor | Short-term | ● Flooding or drought caused by long and intermittent heavy rain, leading to equipment failures in the factory area and resulting in premature demolishment of the assets, the cost of which is estimated to be NT$1,994,080,000 (according to the balance of the fixed asset equipment on the 2023 balance sheet) |

| Physical | Occurrence of floods | ● Northern Vietnam experiences relatively few typhoons, and the location of our company’s factory is at a higher elevation. ● Following the IPCC AR6 SSP scenarios we selected the SSP1-2.6 low-emission pathway (i.e., 1.8 °C warming by 2100) and the SSP5-8.5 high-emission pathway (i.e., 4.4 °C warming by 2100) for physical risk analysis. We fully examined the short-, medium-, and long-term risks of sea-level rise, sea level and floods, and water level effects due to warming. The analysis indicates that our factory area is at low risk. | The Company’s direct operation | Catastrophic | Short-term | ● Flooding or drought caused by long and intermittent heavy rain, leading to equipment failures in the factory area and resulting in premature demolishment of the assets, the cost of which is estimated to be NT$1,994,080,000 (according to the balance of the fixed asset equipment on the 2023 balance sheet) |

| Physical | The rise of average temperature | ● In 2023, the highest temperature in Vietnam was recorded in the Hà Đông district of Hanoi on May 17th at 40°C, with temperatures exceeding 39°C in the provinces of Thanh Hoa, Nghe An, and Hòa Bình. The hot season of Hanoi lasted for 4.8 months from May 4th to September 28th, with daily average temperatures above 31°C. The hottest month in Hanoi is June, with an average high of 33°C and an average low of 26°C. The cold season lasted for 2.6 months from December 11th to February 29th, with daily average temperatures below 22°C. The coldest month in Hanoi is January, with an average low of 14°C and an average high of 20°C. | The Company’s direct operation | Catastrophic | Long-term | ● Flooding or drought caused by long and intermittent heavy rain, leading to equipment failures in the factory area and resulting in premature demolishment of the assets, the cost of which is estimated to be NT$1,994,080,000 (according to the balance of the fixed asset equipment on the 2023 balance sheet) |

| Physical | The rise of sea levels | ● Northern Vietnam experiences relatively few typhoons, and the location of our company’s factory is at a higher elevation. ● Following the IPCC AR6 SSP scenarios we selected the SSP1-2.6 low-emission pathway (i.e., 1.8 °C warming by 2100) and the SSP5-8.5 high-emission pathway (i.e., 4.4 °C warming by 2100) for physical risk analysis. We fully examined the short-, medium-, and long-term risks of sea-level rise, sea level and floods, and water level effects due to warming. The analysis indicates that our factory area is at low risk. | The Company’s direct operation | Catastrophic | Long-term | ● Flooding or drought caused by long and intermittent heavy rain, leading to equipment failures in the factory area and resulting in premature demolishment of the assets, the cost of which is estimated to be NT$1,994,080,000 (according to the balance of the fixed asset equipment on the 2023 balance sheet) |

| Physical | Severe Water Shortage | ● There is a reservoir in our factory area to prevent operational disruptions caused by drought and water shortages. ● Based on IPCC AR6 SSP scenario, the Company regards the pressure of water scarcity for our factory area as moderate to low risk before 2050 under the SSP1-2.6 (optimistic) and SSP5-8.5 (pessimistic) scenarios. | The Company’s direct operation | Minor | Long-term | ● lThe long-term drought caused by changes in rainfall patterns will affect the stability of water supply for the factory, leading to operational disruptions (painting production line). We will need to purchase water externally at a cost of approximately 13,333 Vietnamese Dong per cubic meter (around NT$17.44). The daily water consumption is approximately 584 cubic meters. Therefore, if there is a water shortage leading to an interruption, the daily operating cost will increase by 7,786,472 Vietnamese Dong (around NT$10,185). |

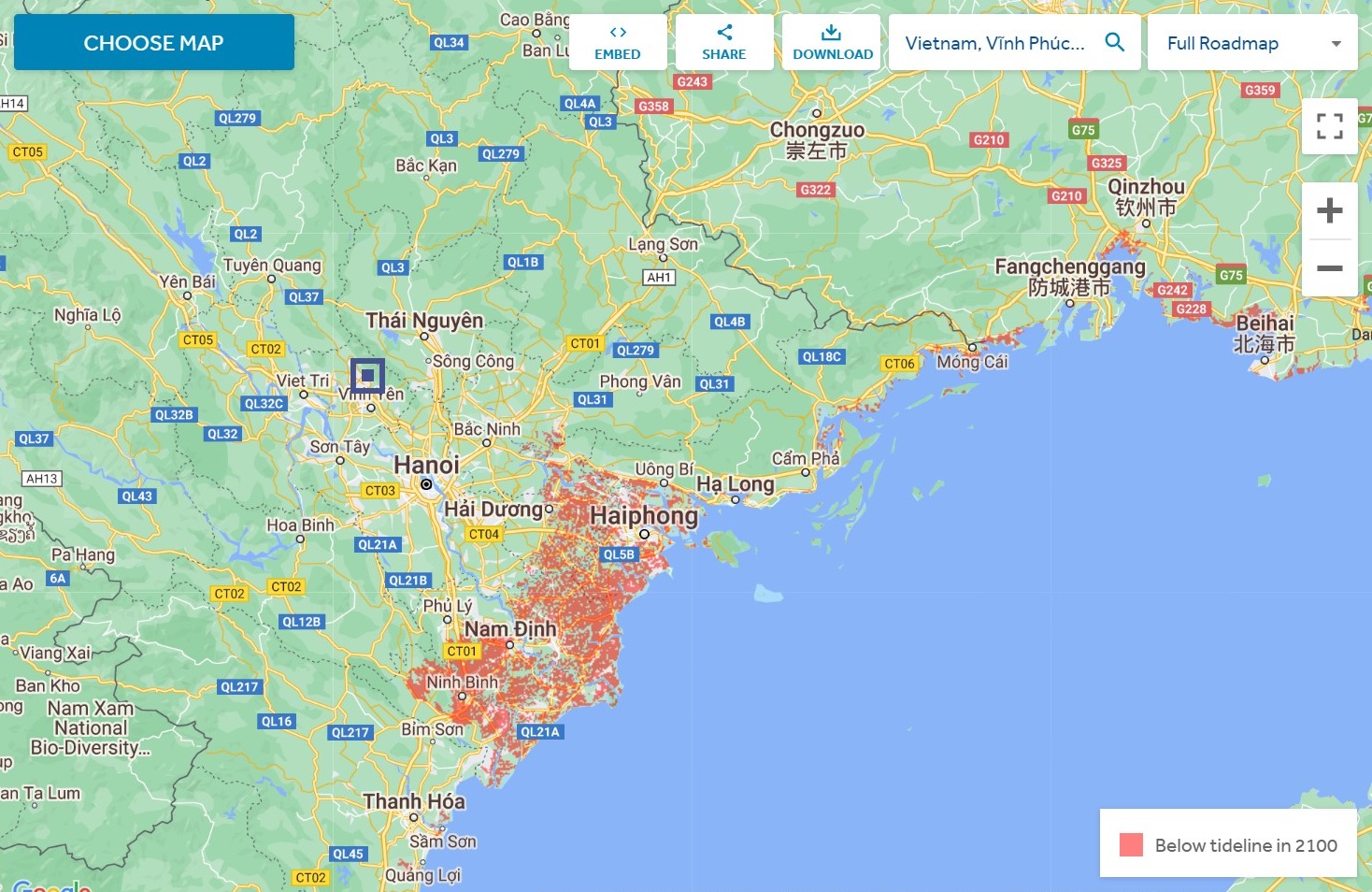

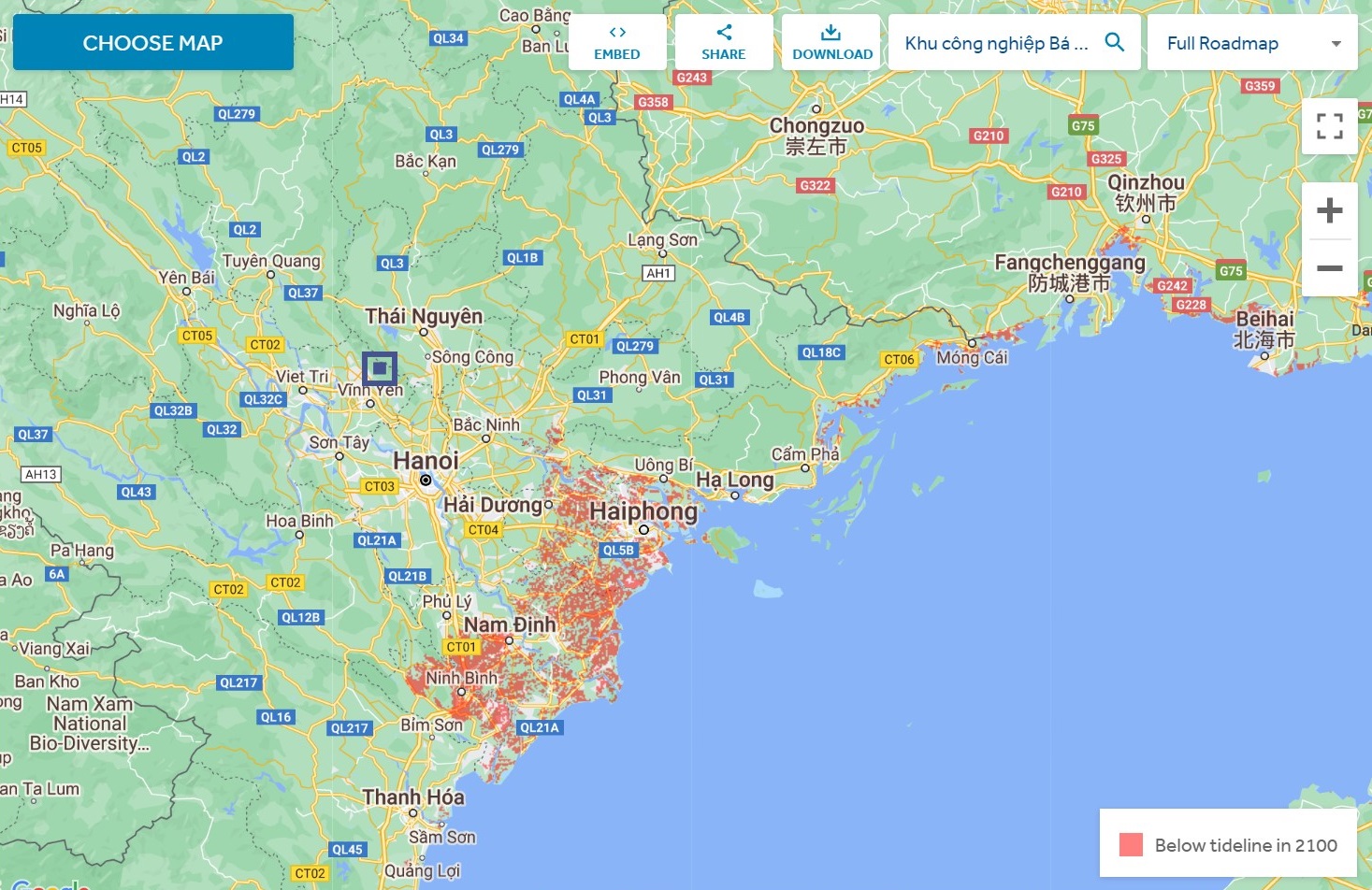

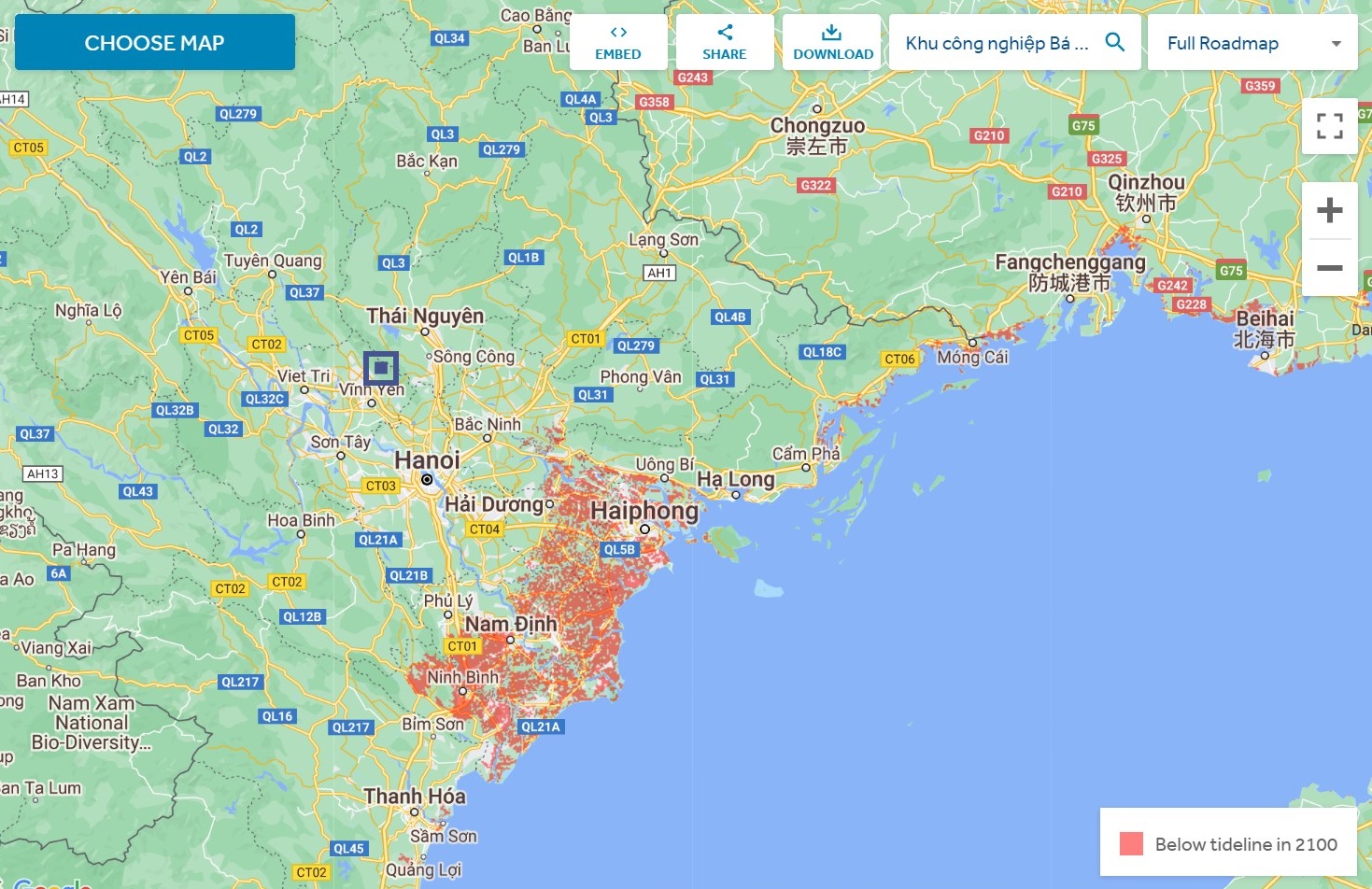

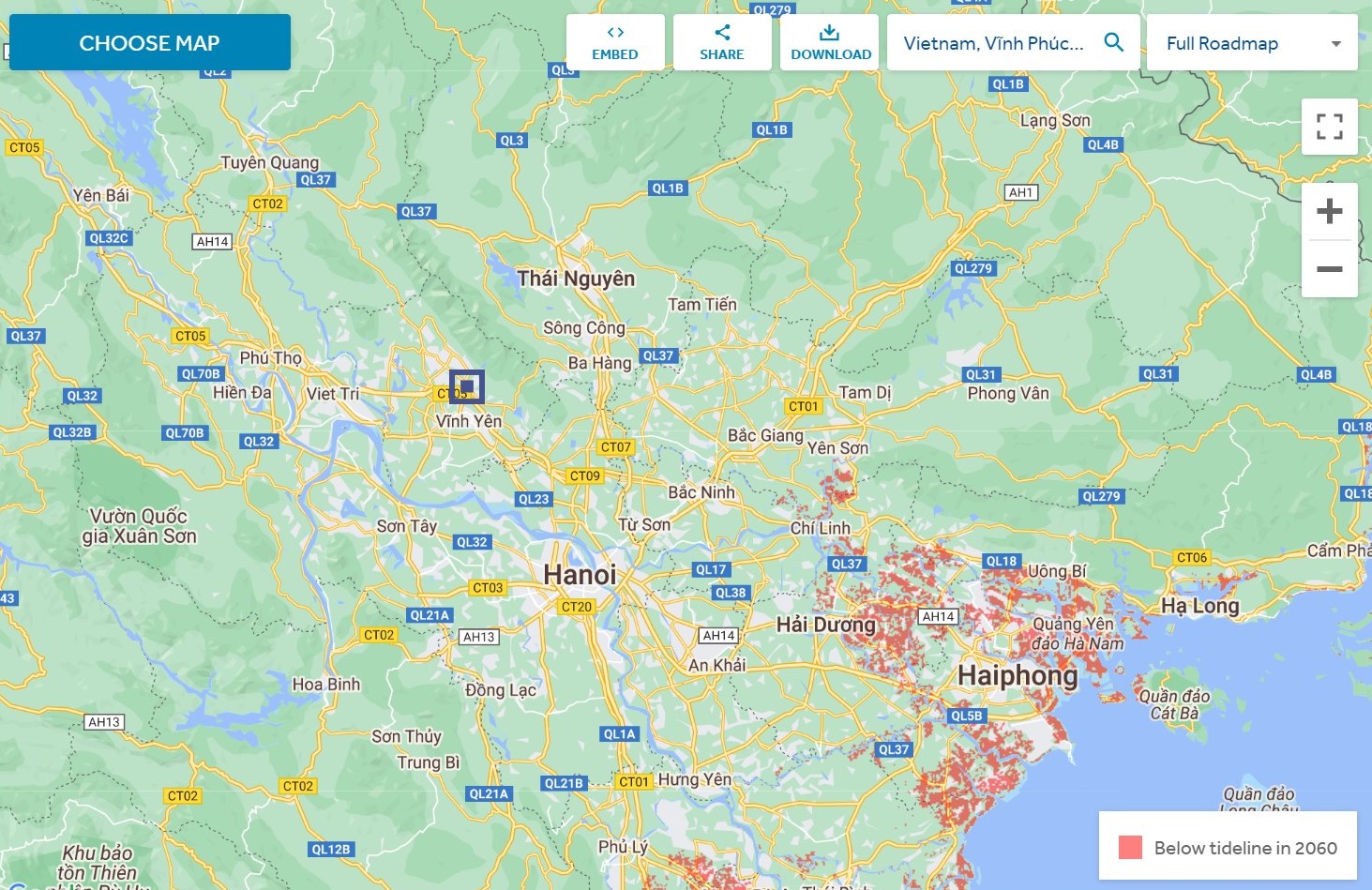

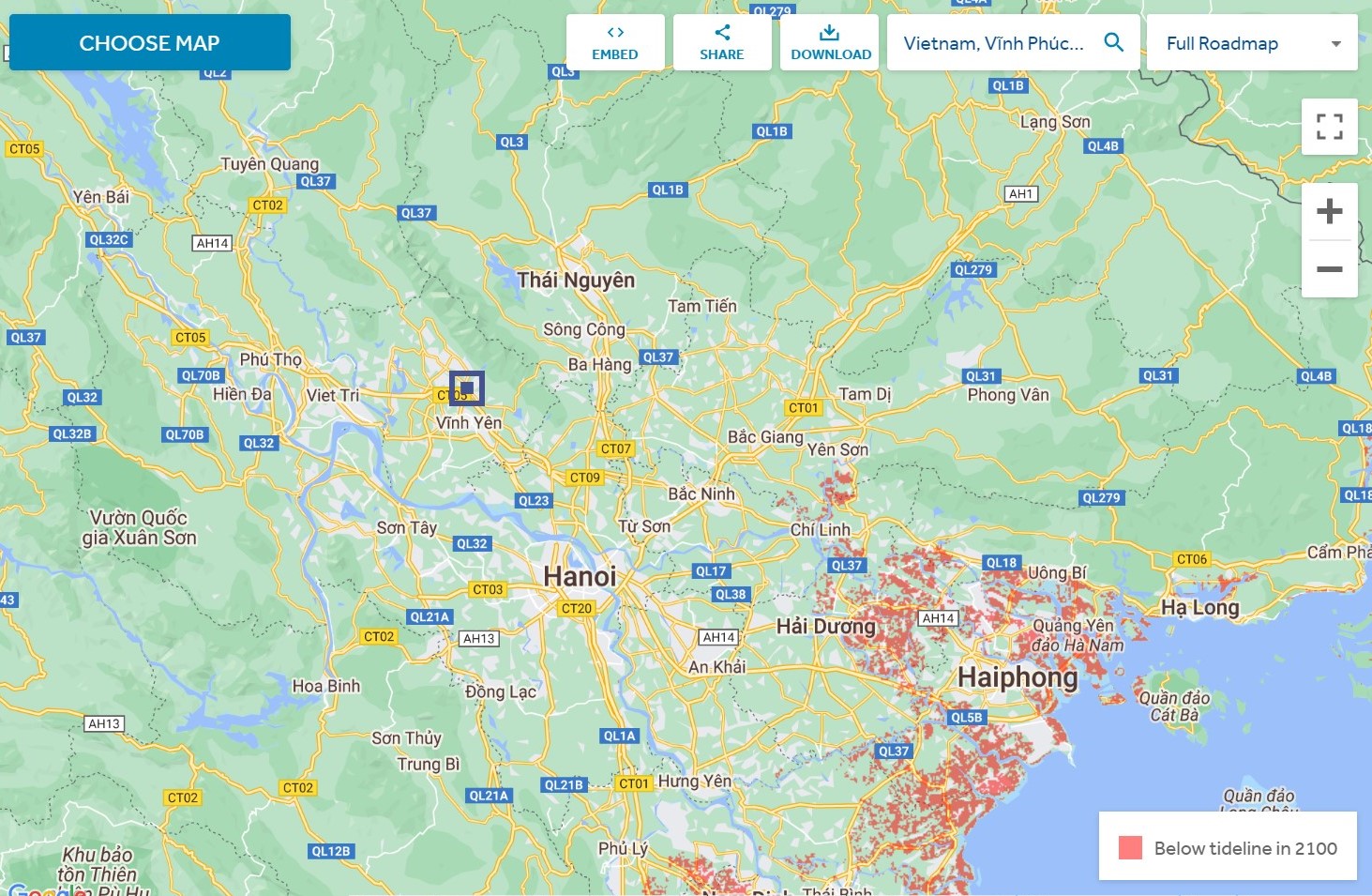

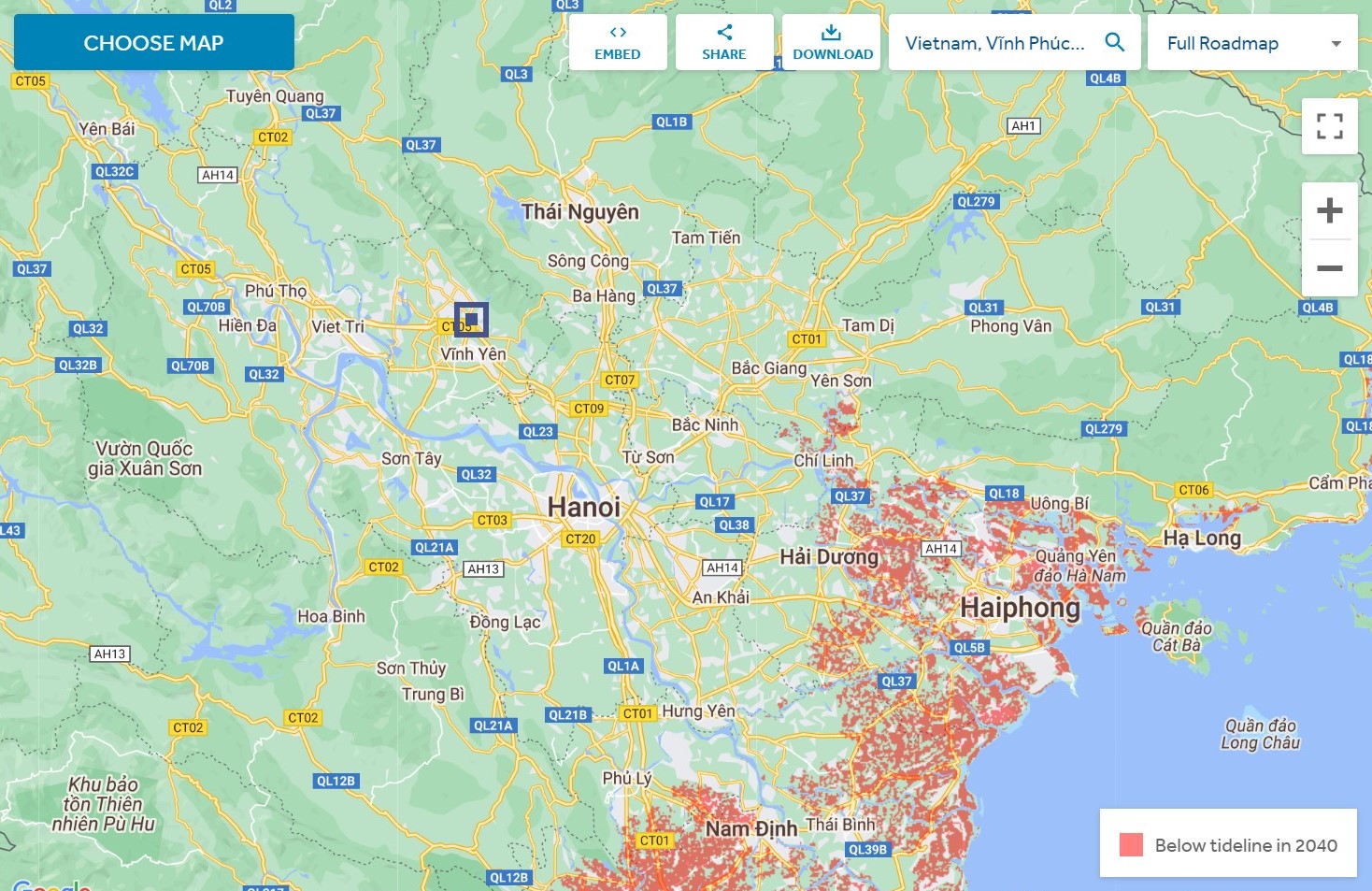

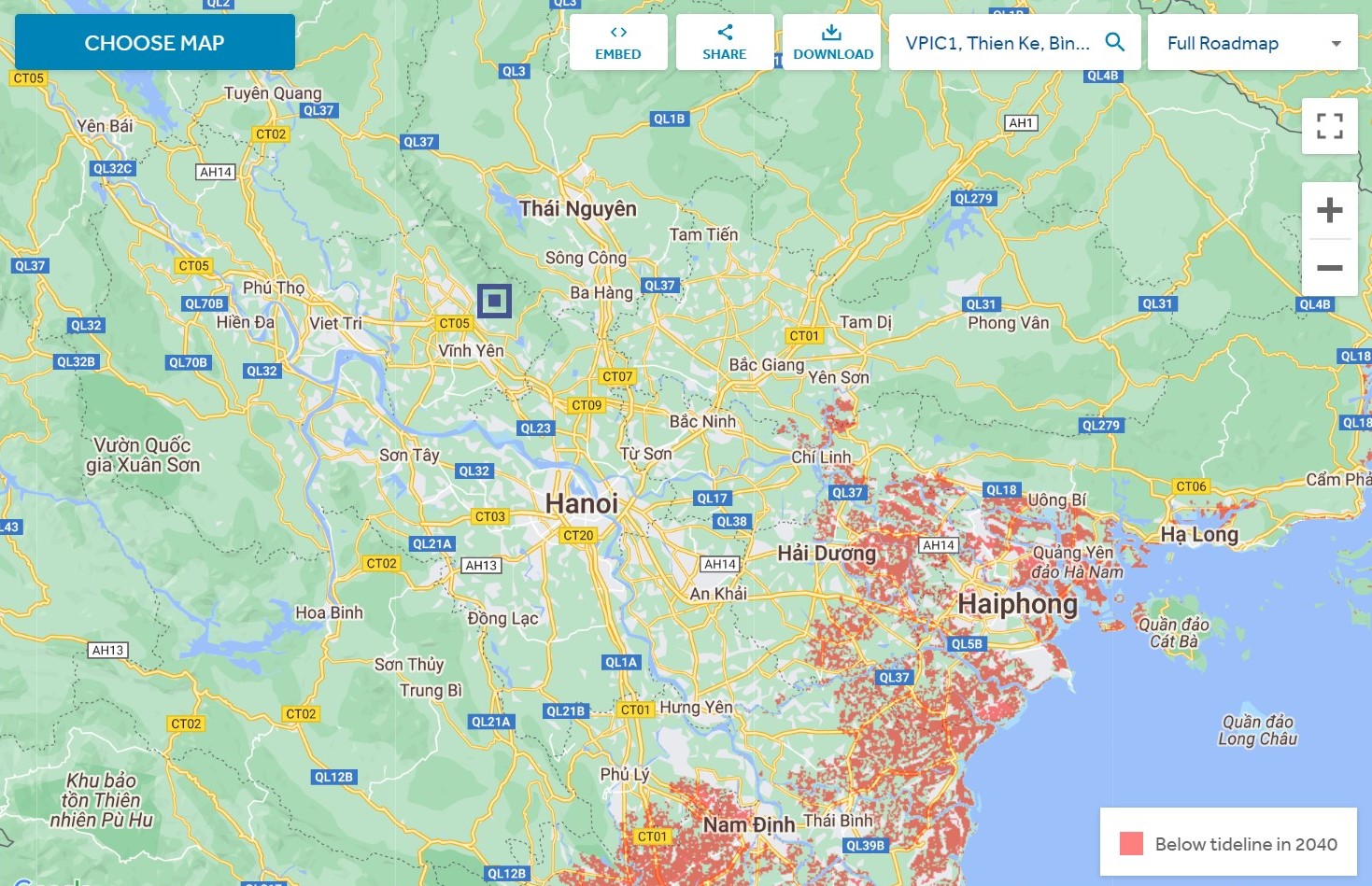

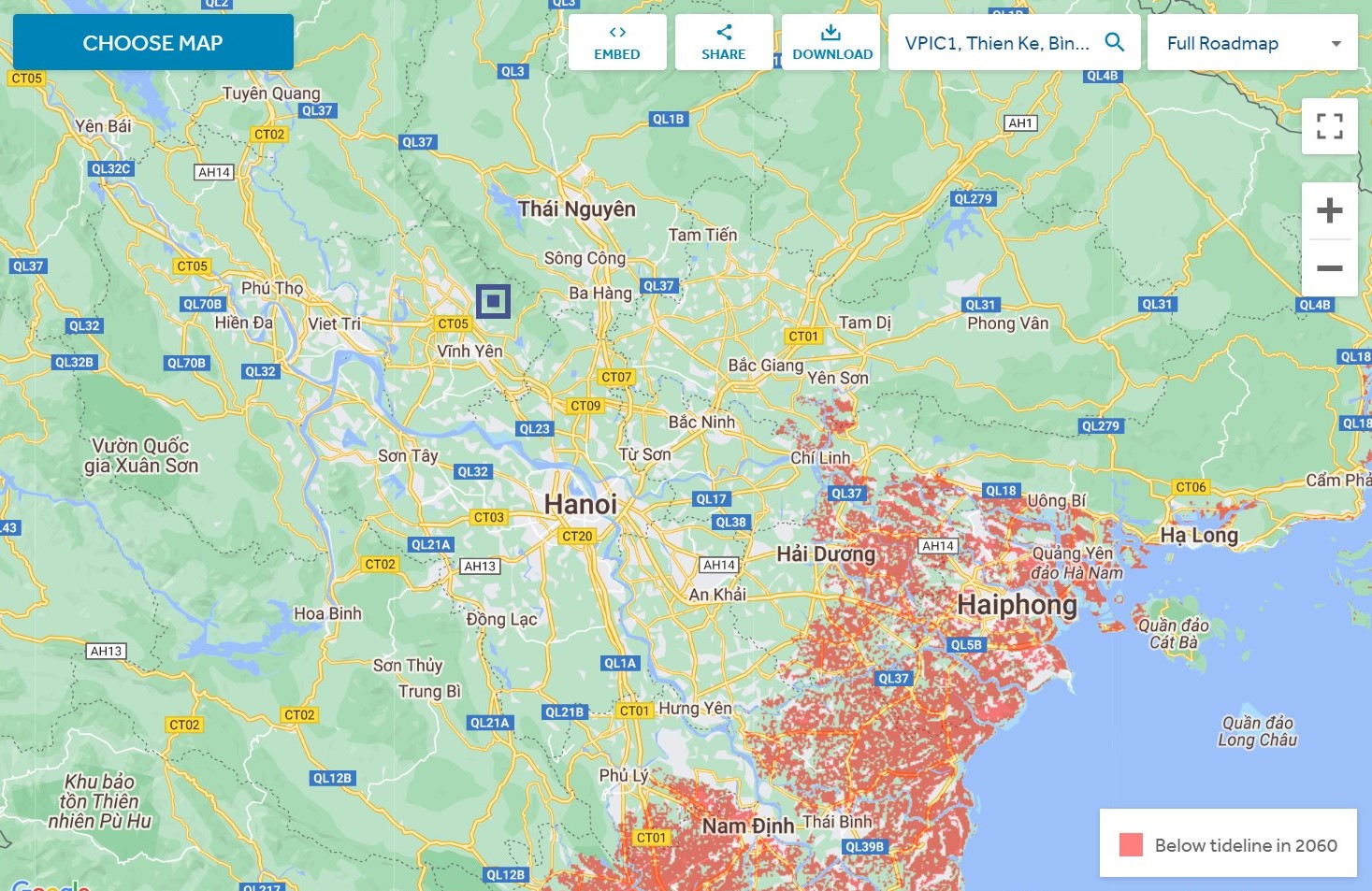

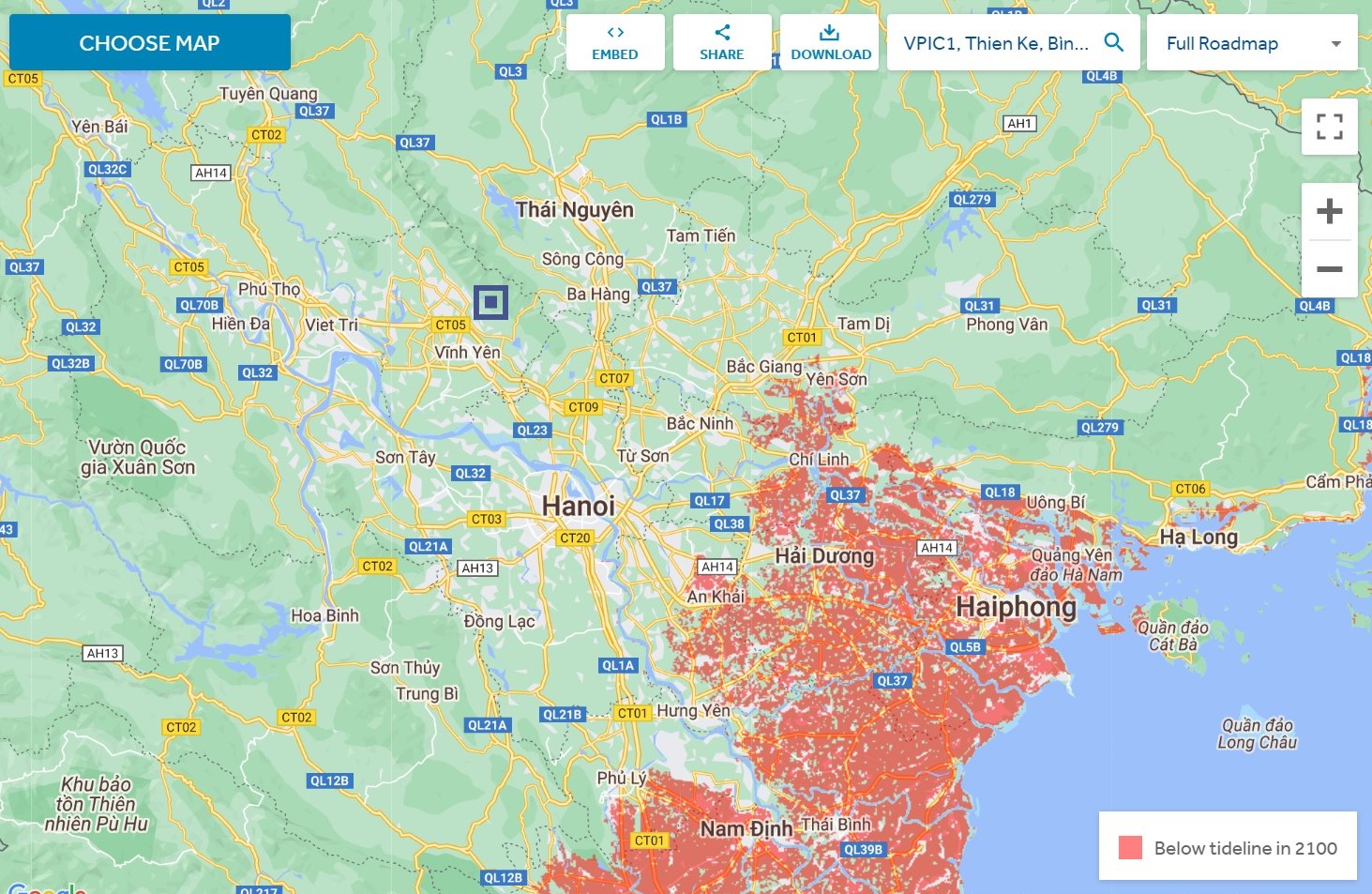

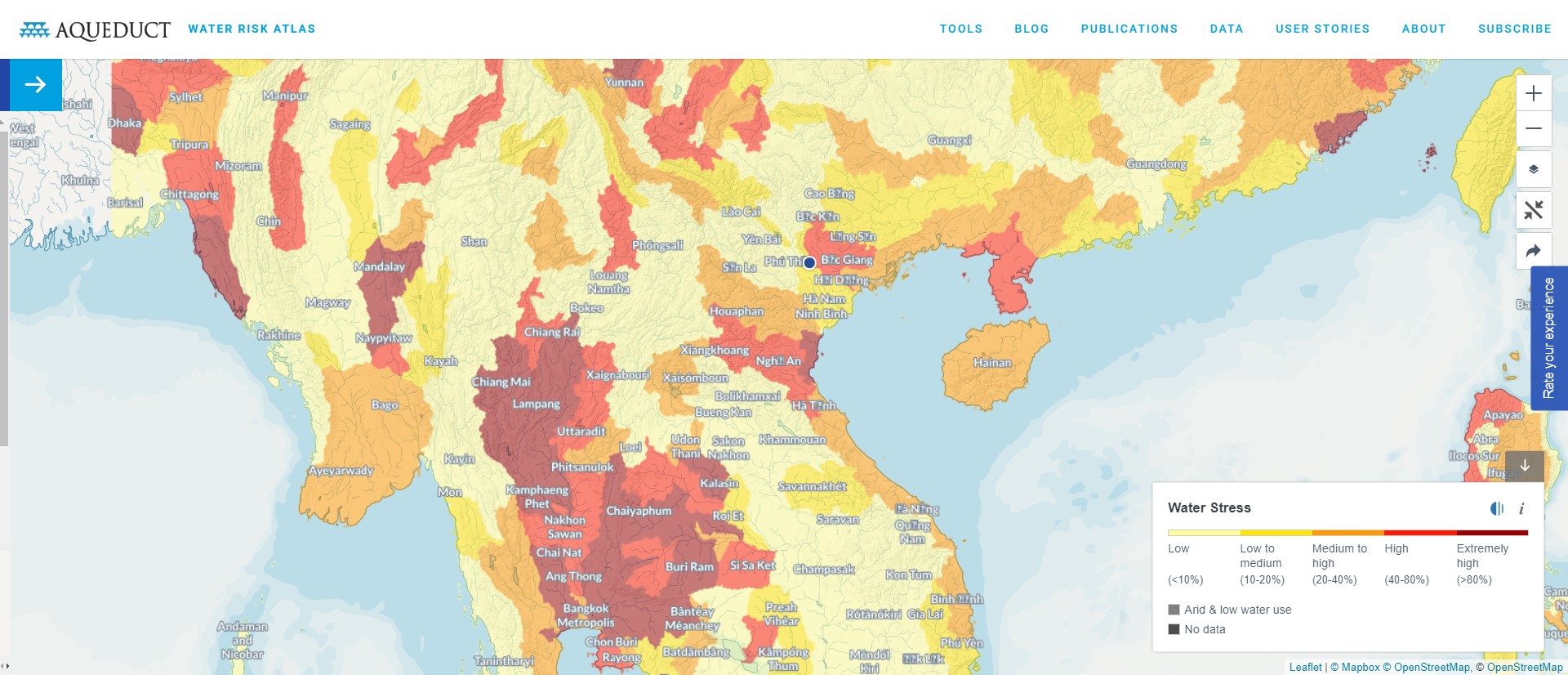

Impact of Sea Levels

| Scenario Assumption | Factory Location | Scenario Assumption | Factory Location |

|---|---|---|---|

| SSP1-2.6 Low-emission pathway (1.8 °C warming by 2100) |  Taiwan | SSP5-8.5 High-emission pathway (4.4 °C warming by 2100) |  Taiwan |

| SSP1-2.6 Low-emission pathway (1.8 °C warming by 2100) |  Vietnam (Khai Quang Industrial Zone) | SSP5-8.5 High-emission pathway (4.4 °C warming by 2100) |  Vietnam (Khai Quang Industrial Zone) |

| SSP1-2.6 Low-emission pathway (1.8 °C warming by 2100) |  Vietnam (Bai-Shan II Industrial Park) | SSP5-8.5 High-emission pathway (4.4 °C warming by 2100) |  Vietnam (Bai-Shan II Industrial Park) |

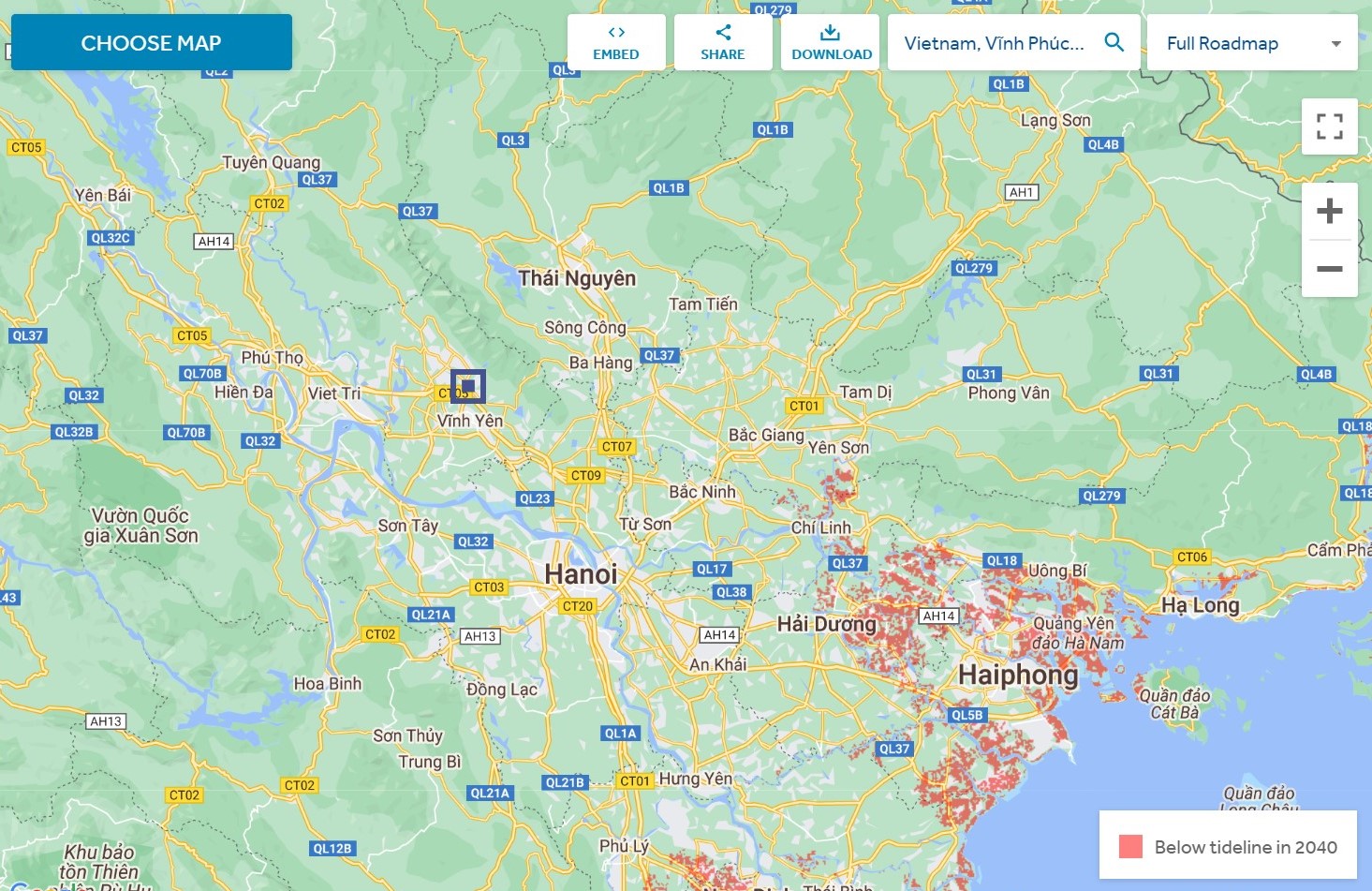

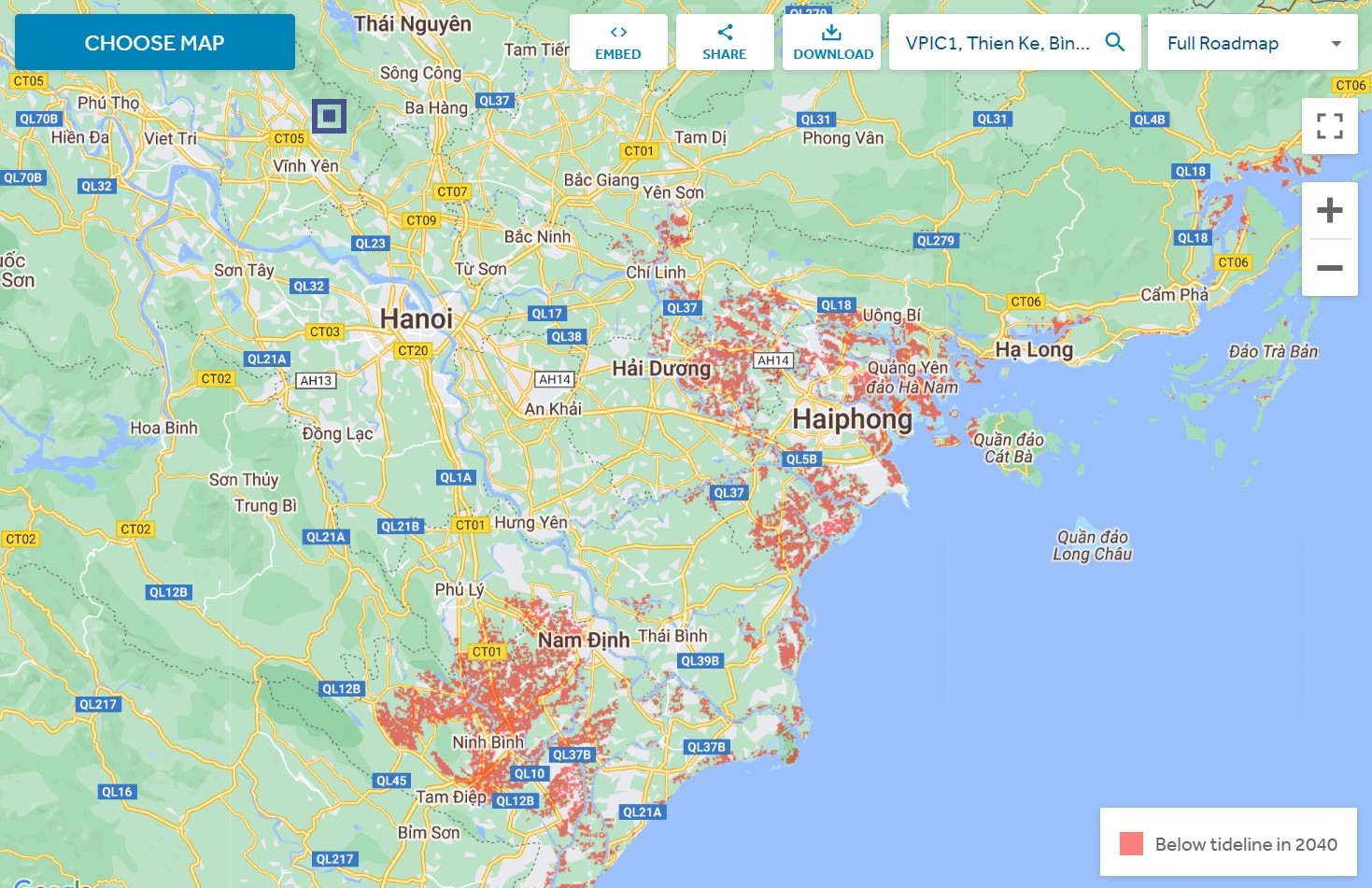

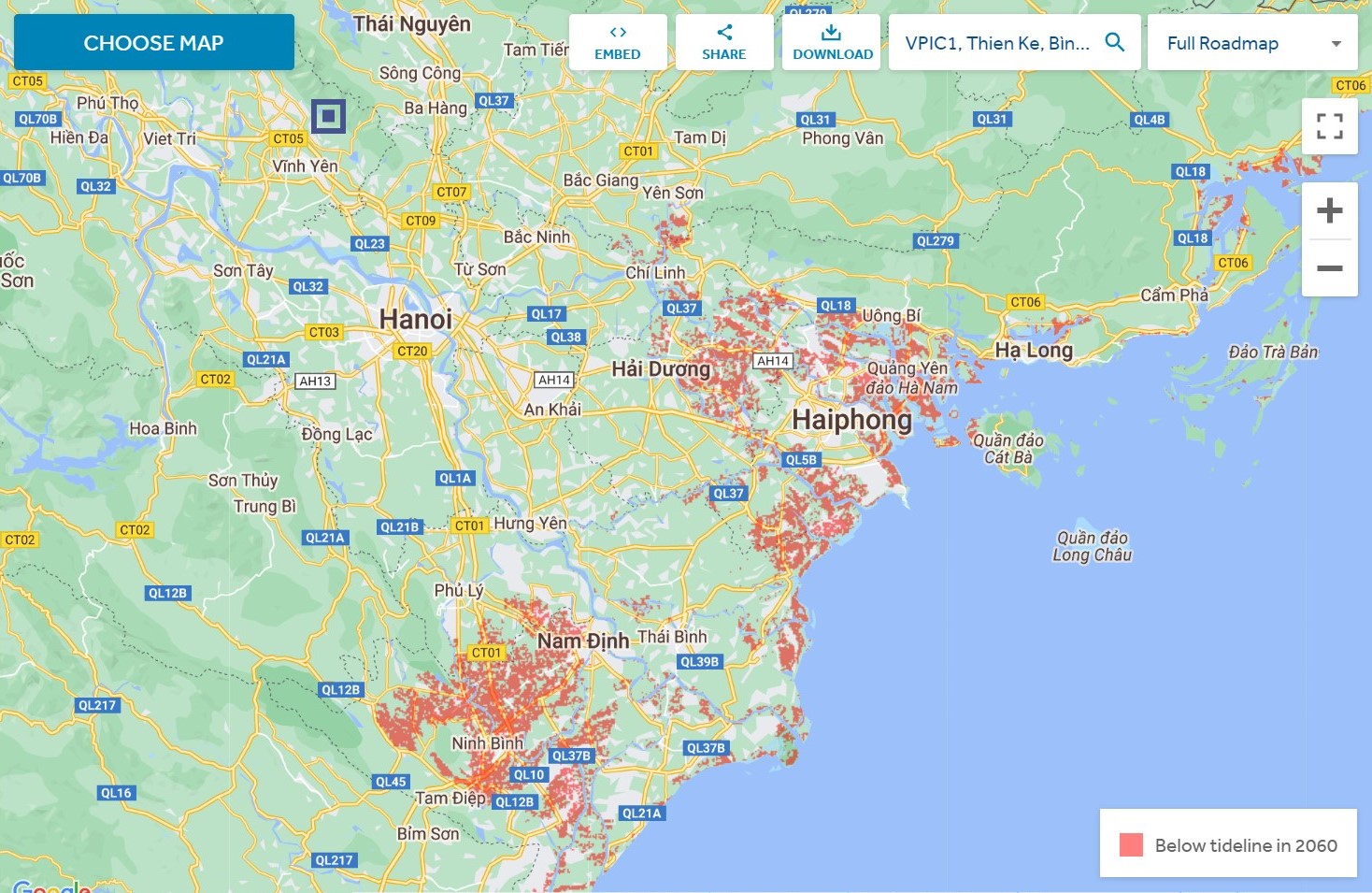

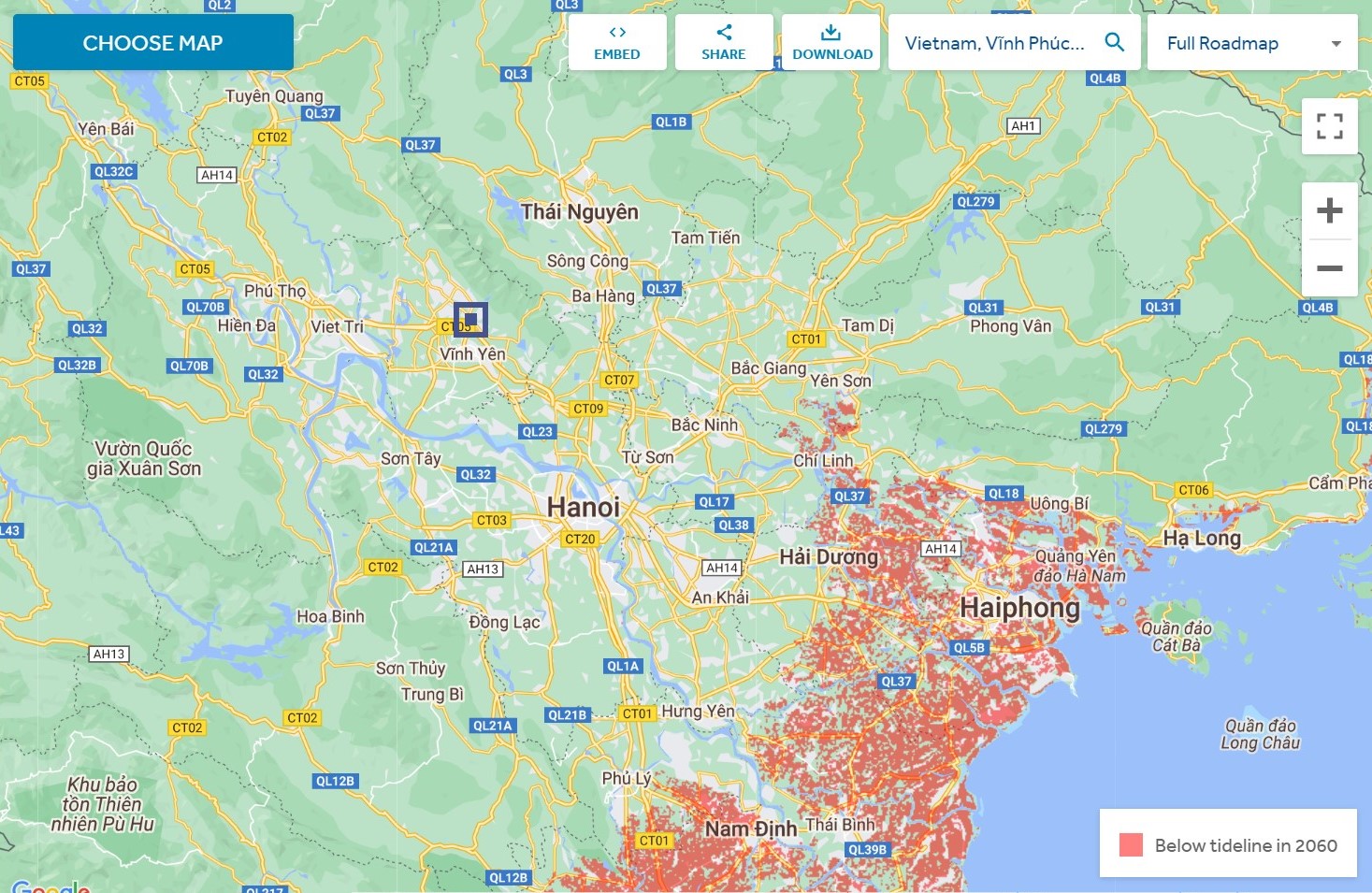

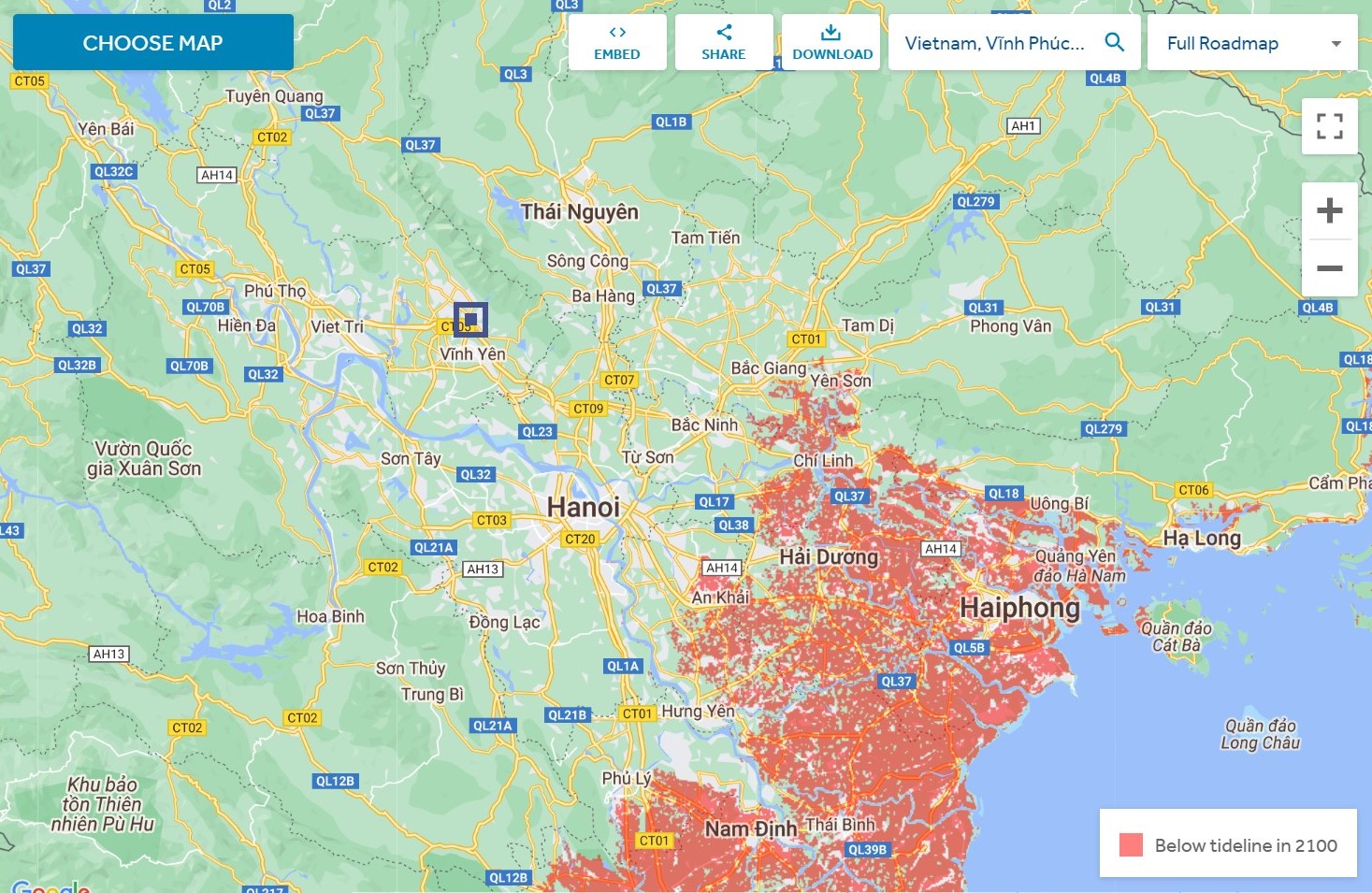

Impact of Sea Levels and Floods

| Scenario Assumption | Factory Location | Estimated temperature rise by 1.5 degree: near future (2021-2040) (Highly probable temperature rise range falls between 1.2 and 1.8.) | Estimated temperature rise by 1.7 degree: mid-term (2041-2060) (Highly probable temperature rise range falls between 1.3 and 2.2.) | Estimated temperature rise by 1.8 degree: mid-term (2081-2100) (Highly probable temperature rise range falls between 1.3 and 2.4.) |

|---|---|---|---|---|

| SSP1-2.6 Low-emission pathway | Taiwan |  |  |  |

| SSP1-2.6 Low-emission pathway | Vietnam (Khai Quang Industrial Zone) |  |  |  |

| SSP1-2.6 Low-emission pathway | Vietnam (Bai-Shan II Industrial Park) |  |  | |

| Scenario Assumption | Factory Location | Estimated temperature rise by 1.6 degree: near future (2021-2040) (Highly probable temperature range falls between 1.2 and 1.9.) | Estimated temperature rise by 2.4 degree: mid-term (2041-2060) (Highly probable temperature range falls between 1.9 and 3.0.) | Estimated temperature rise by 4.4 degree: long-term (2081-2100) (Highly probable temperature range falls between 3.3 and 5.7.) |

|---|---|---|---|---|

| SSP5-8.5 High-emission pathway | Taiwan |  |  |  |

| SSP5-8.5 High-emission pathway | Vietnam (Khai Quang Industrial Zone) |  |  |  |

| SSP5-8.5 High-emission pathway | Vietnam (Bai-Shan II Industrial Park) |  |  |  |

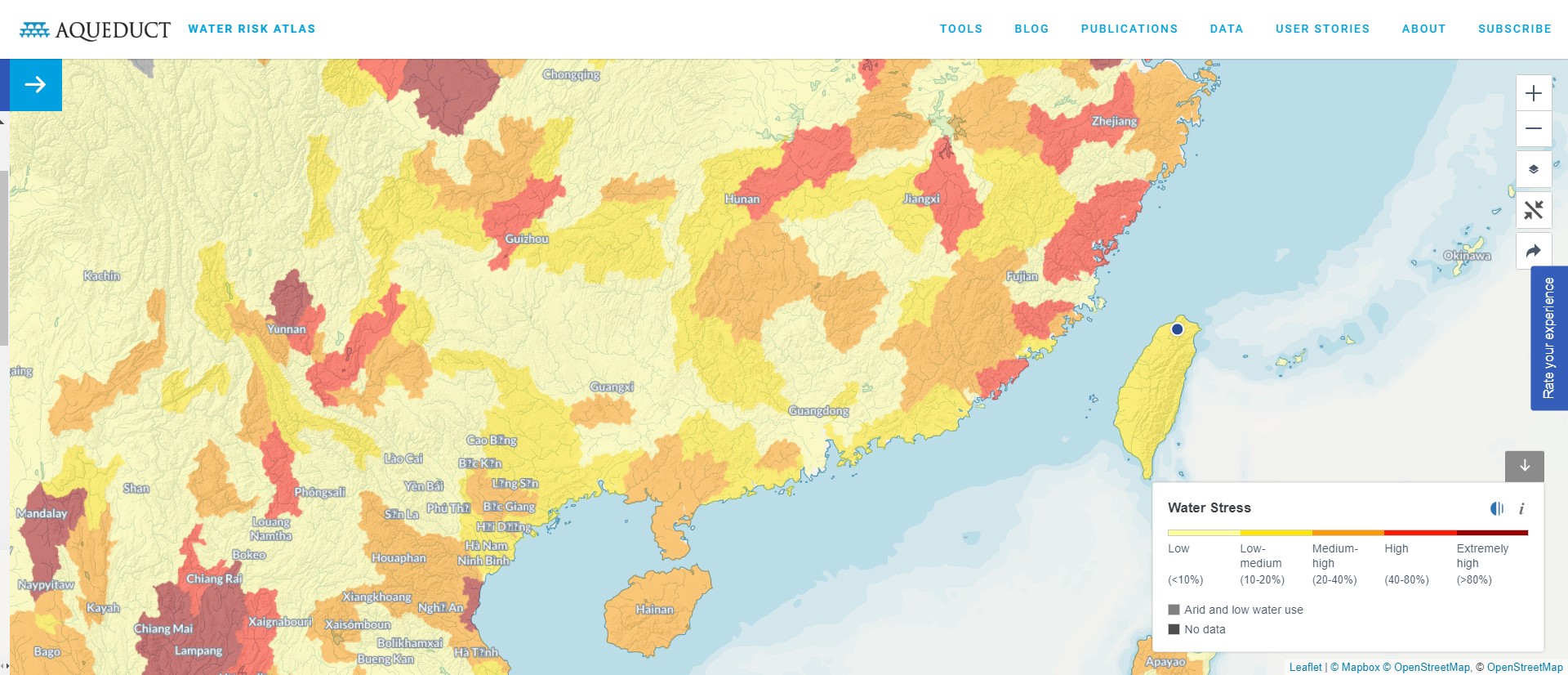

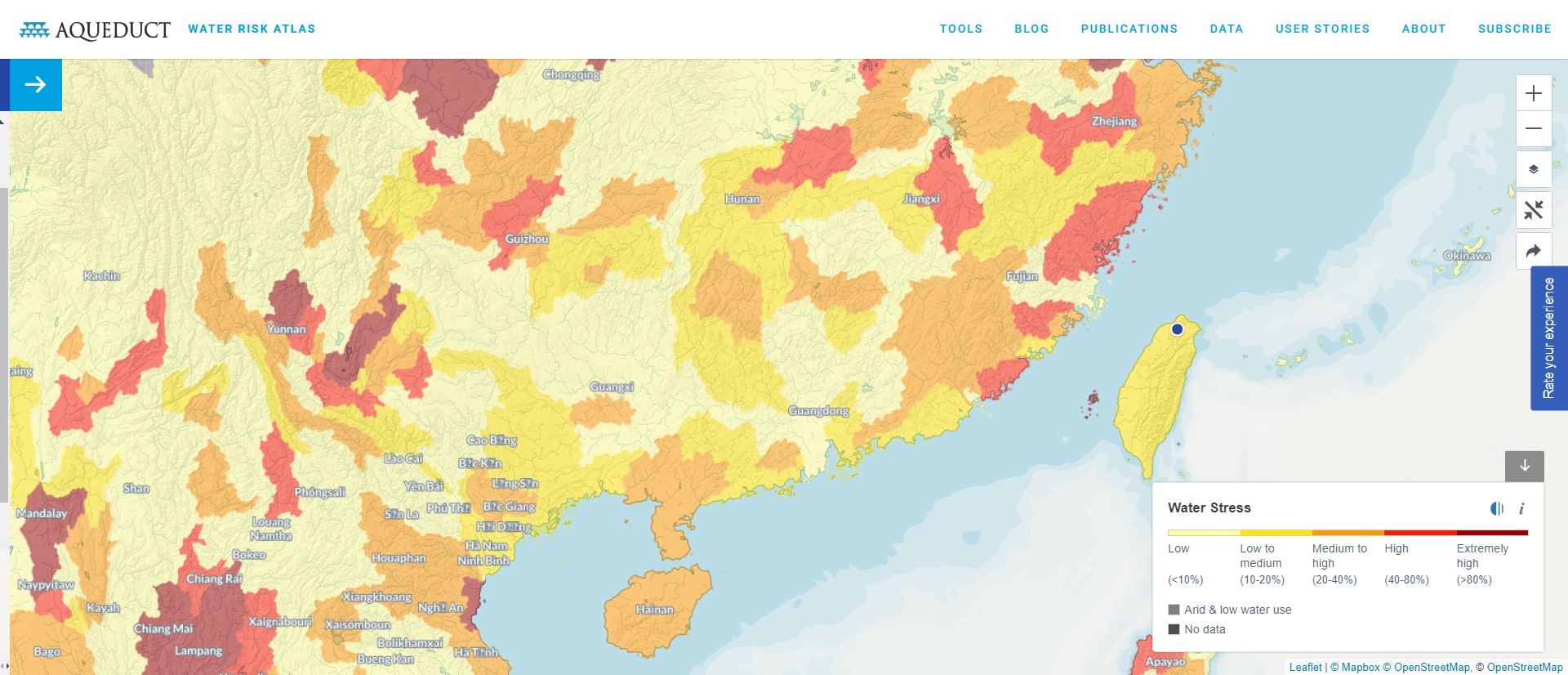

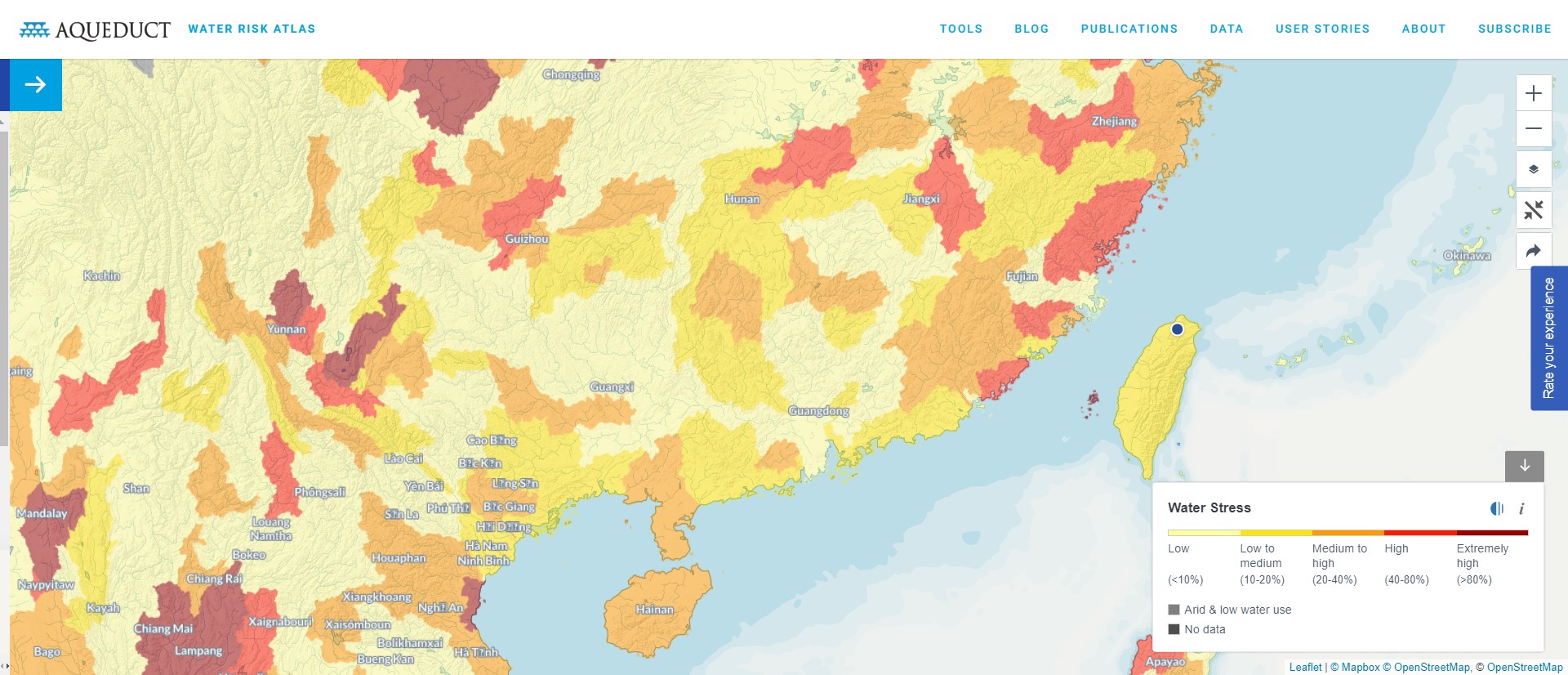

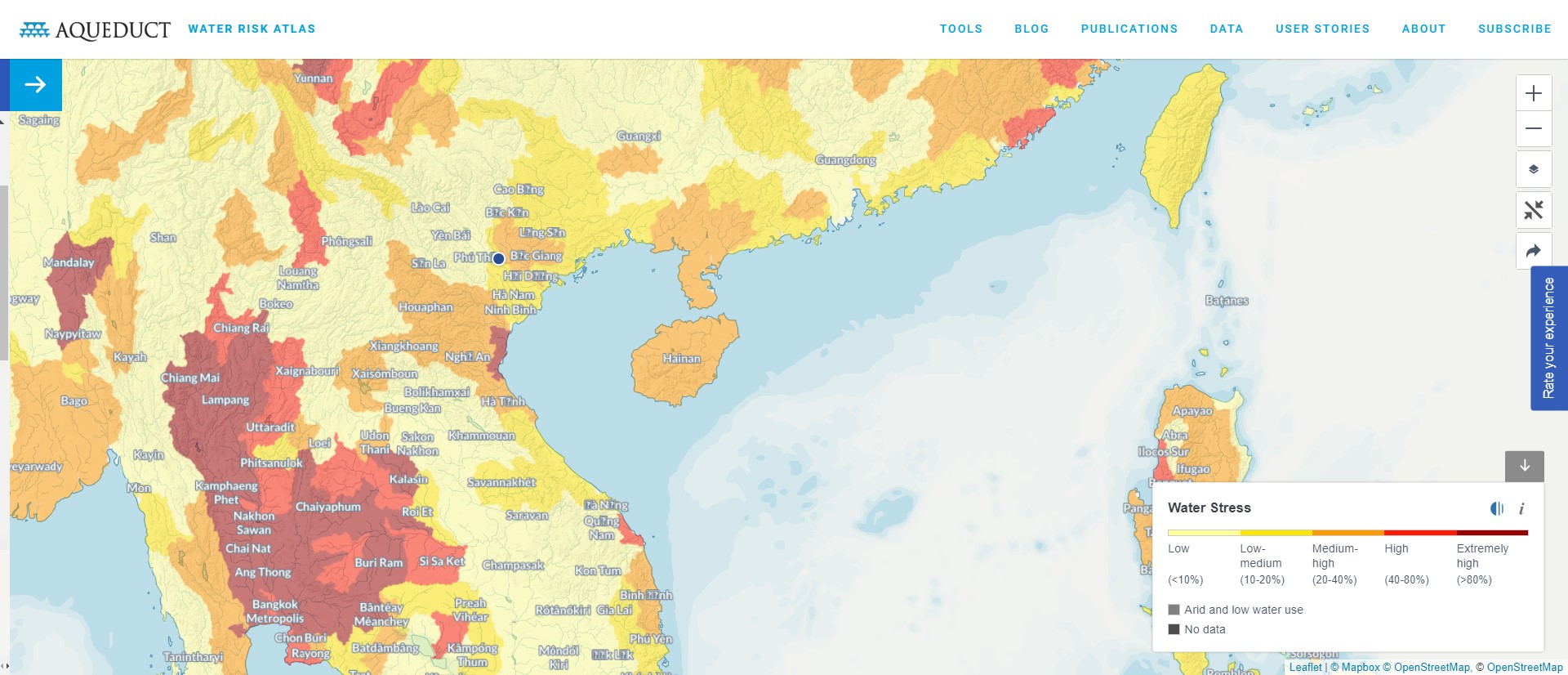

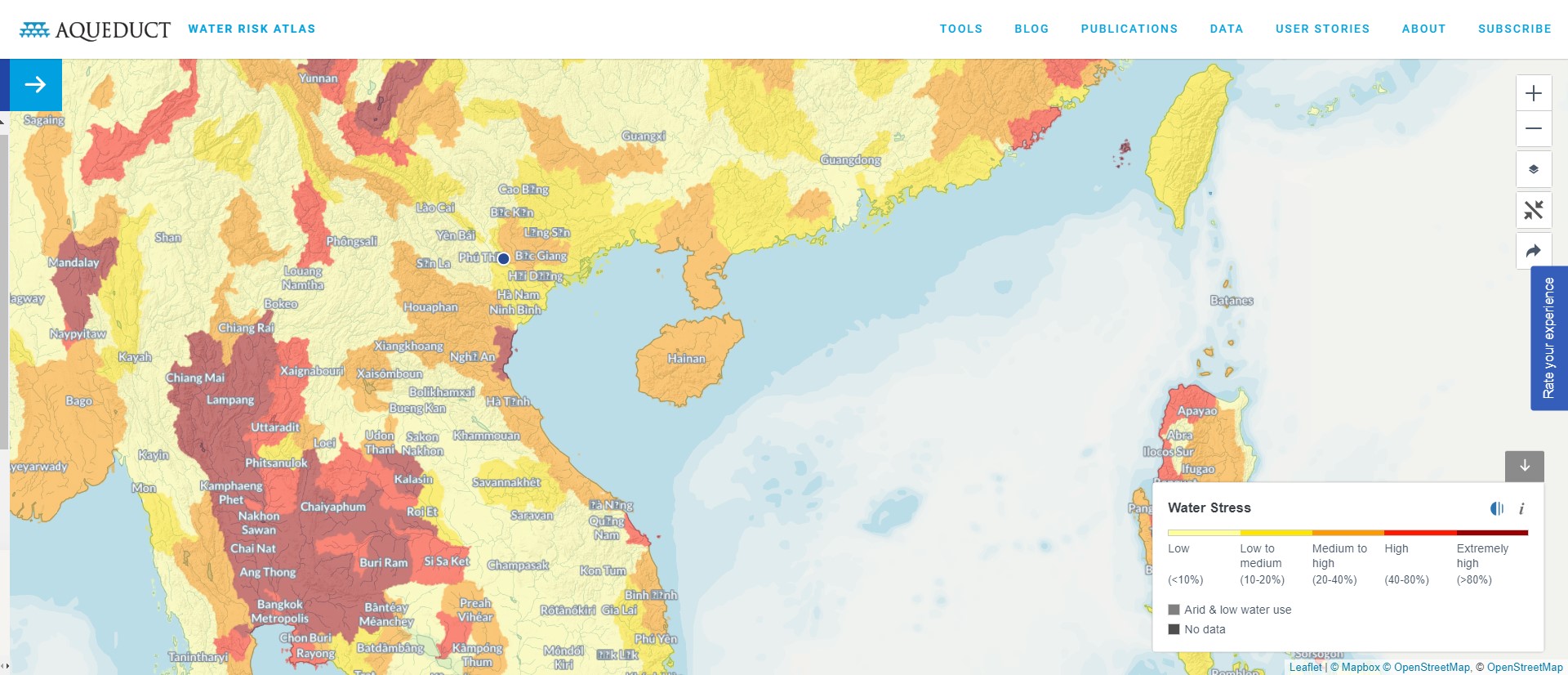

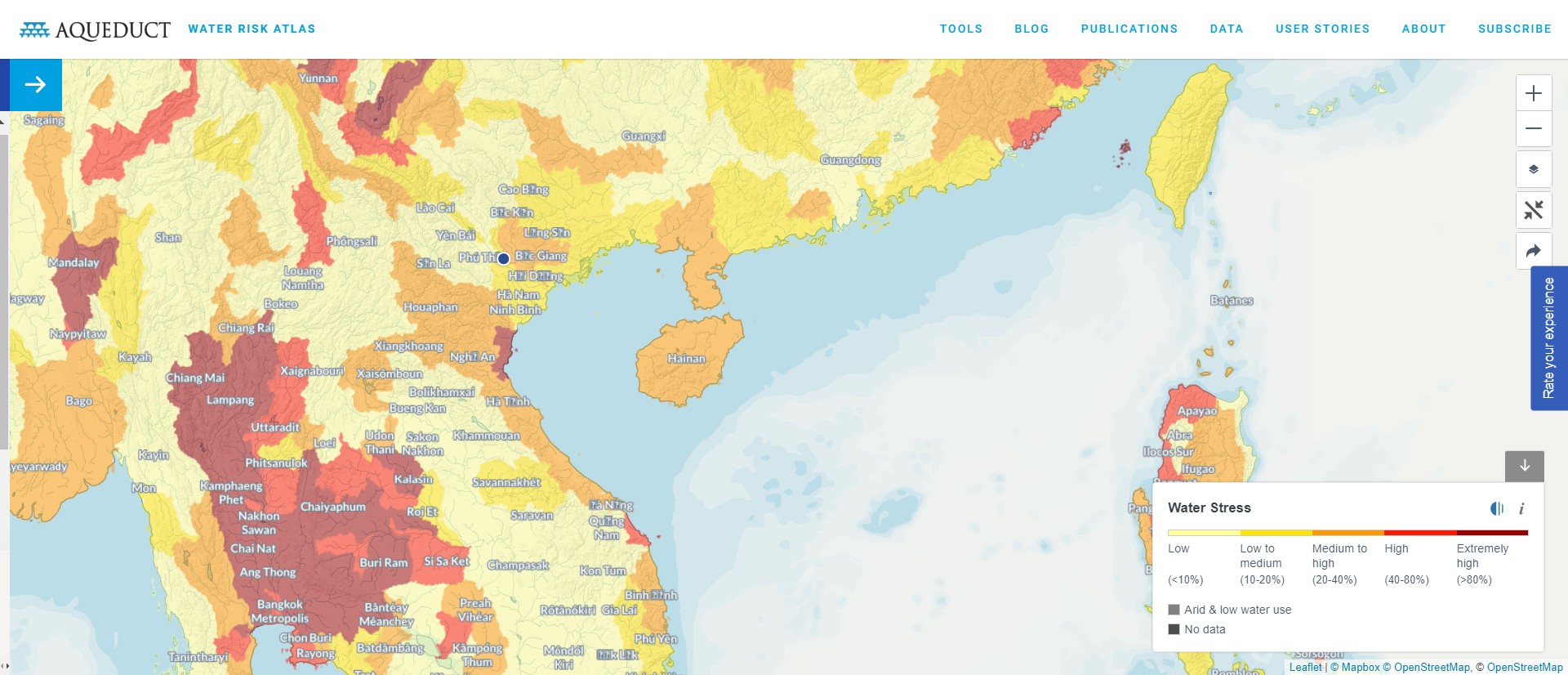

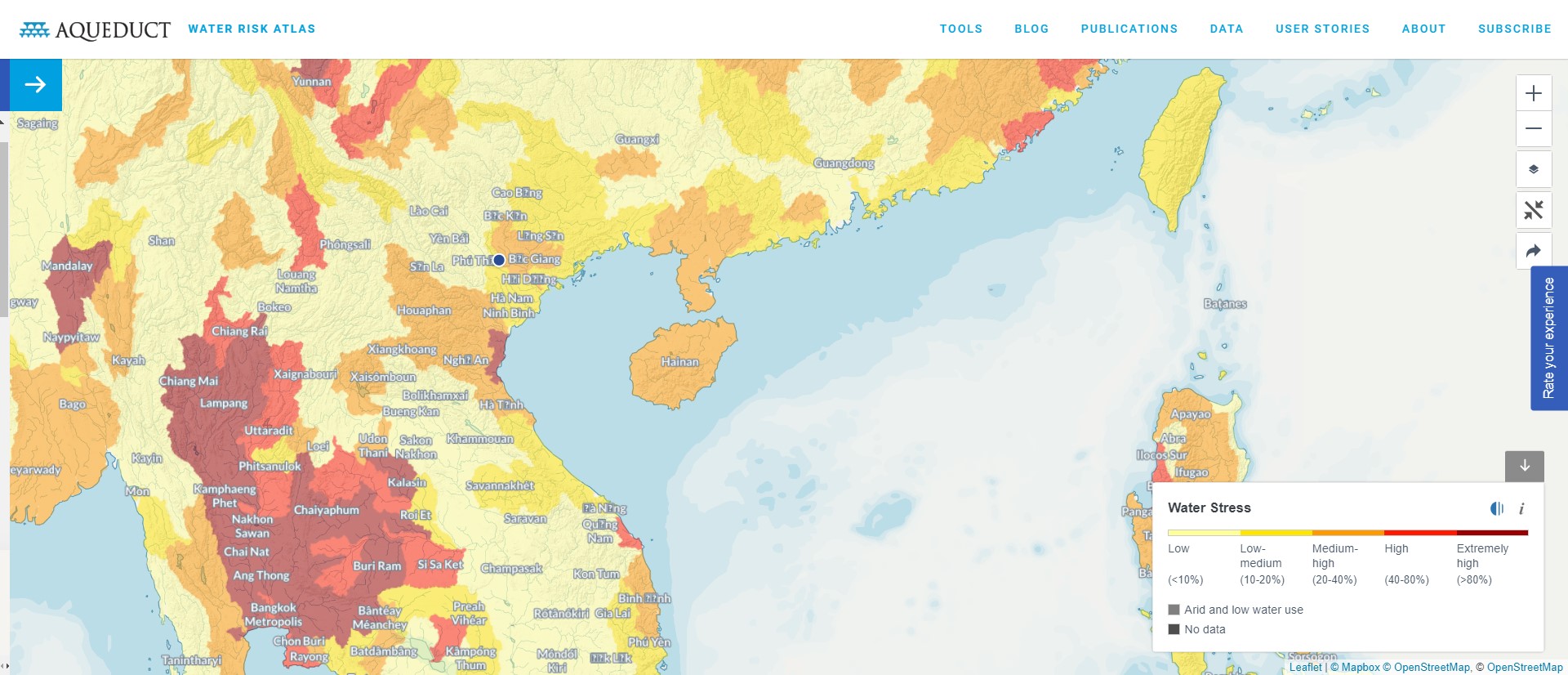

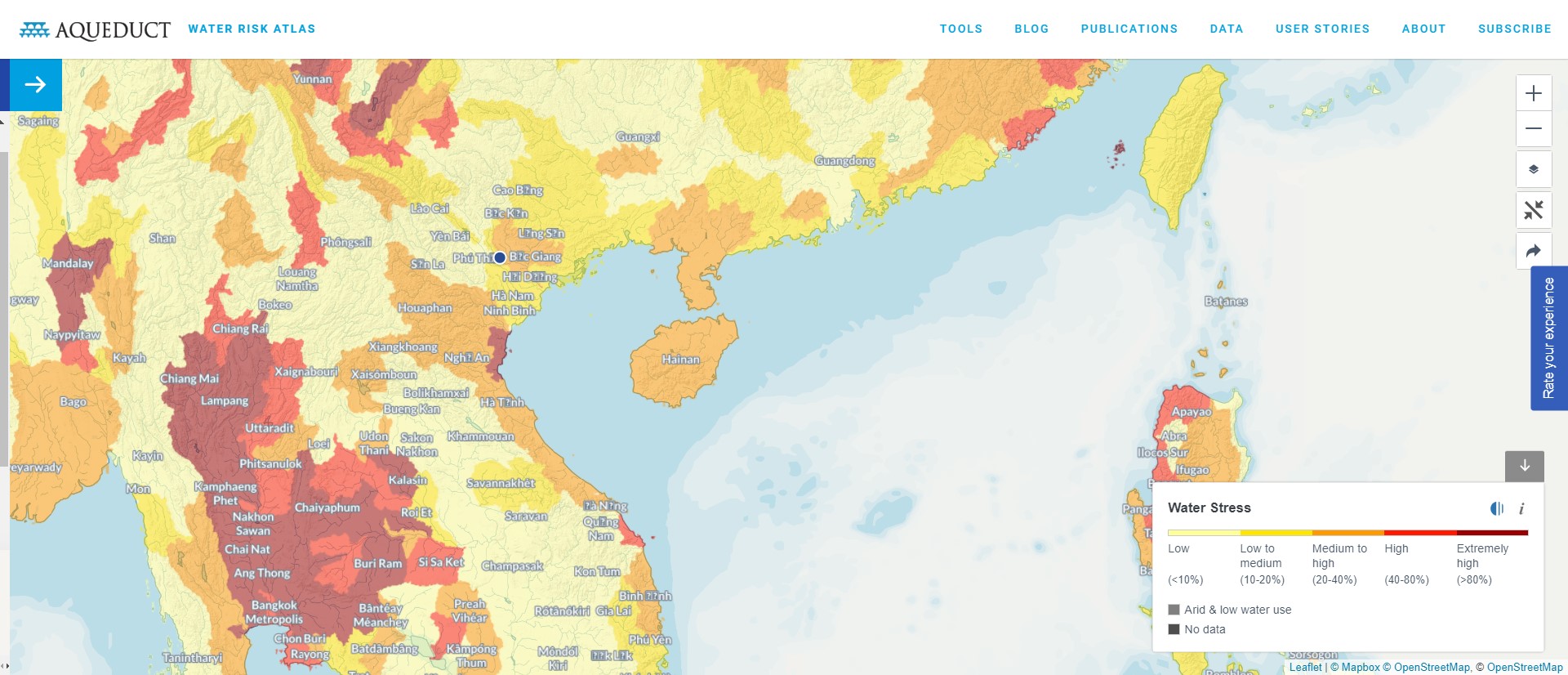

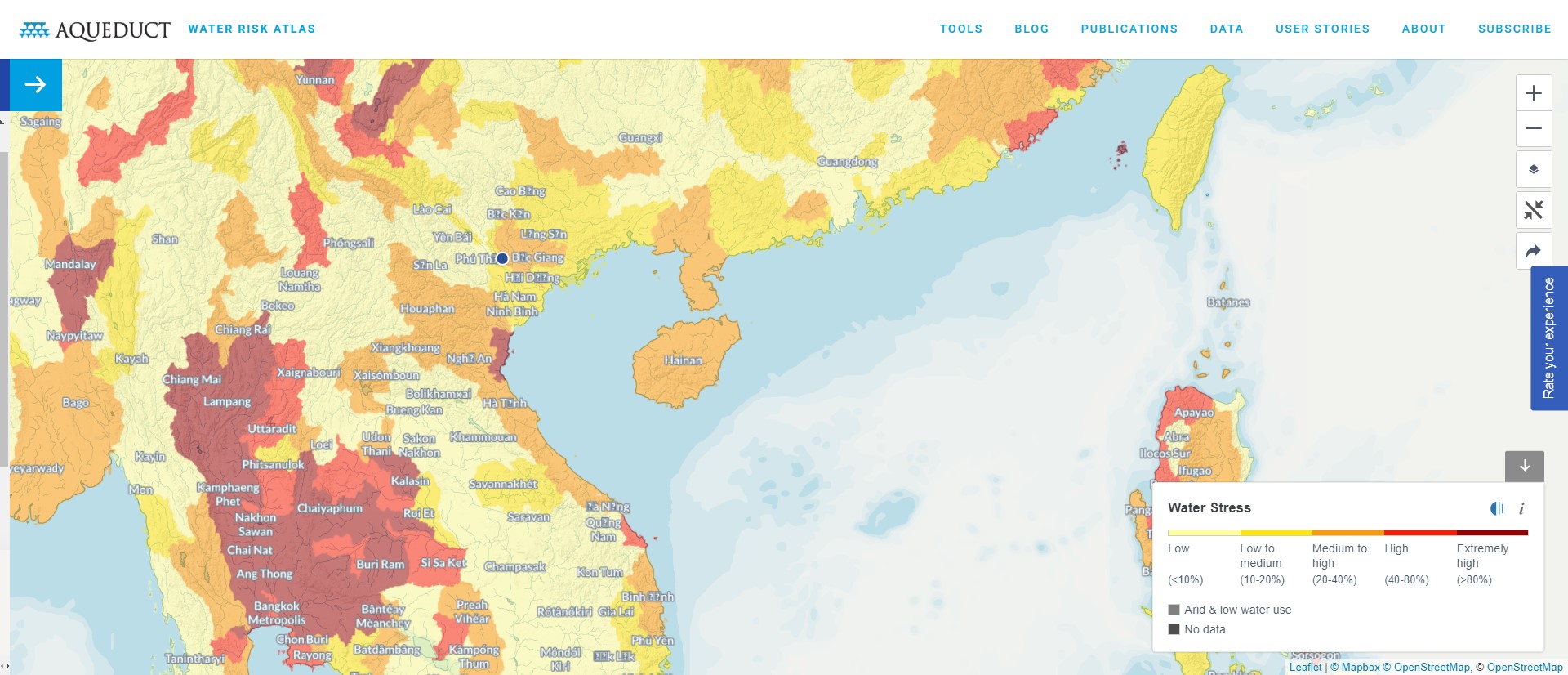

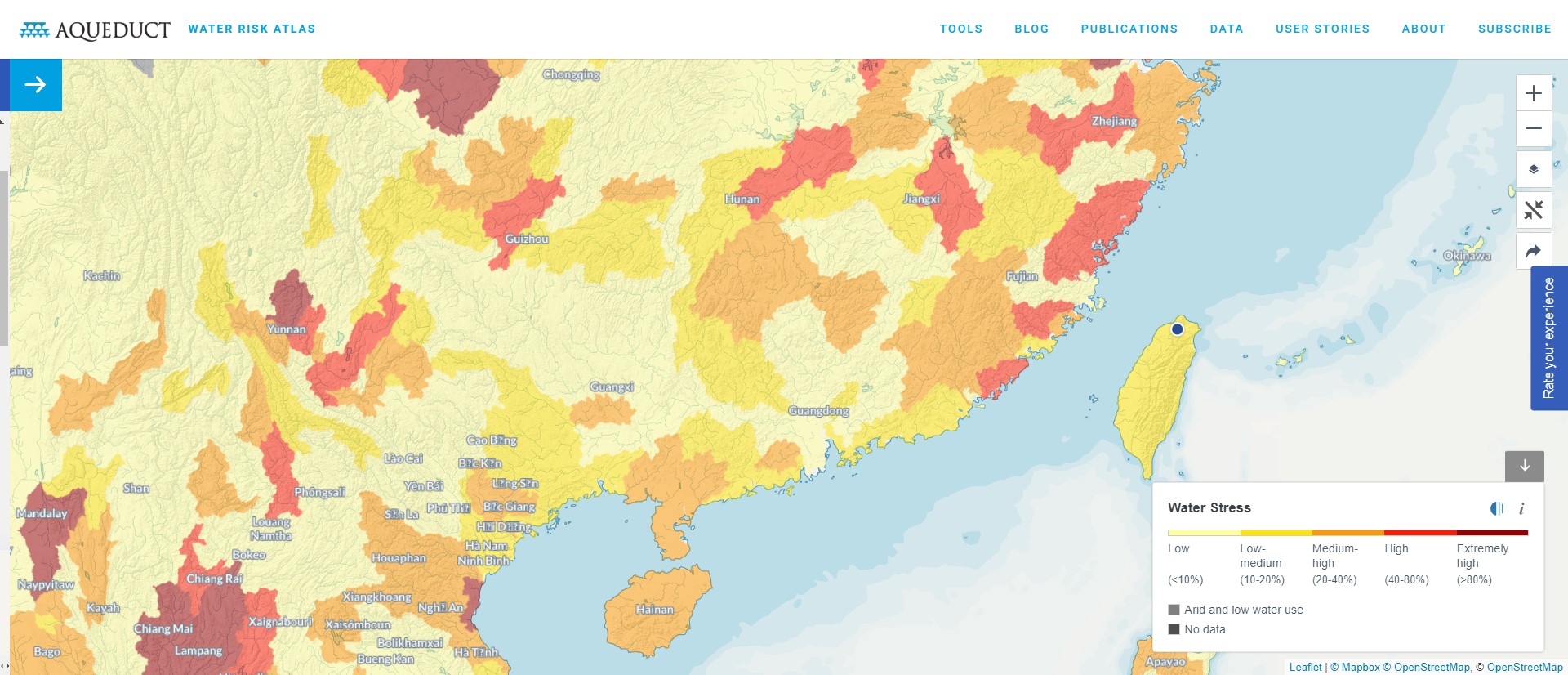

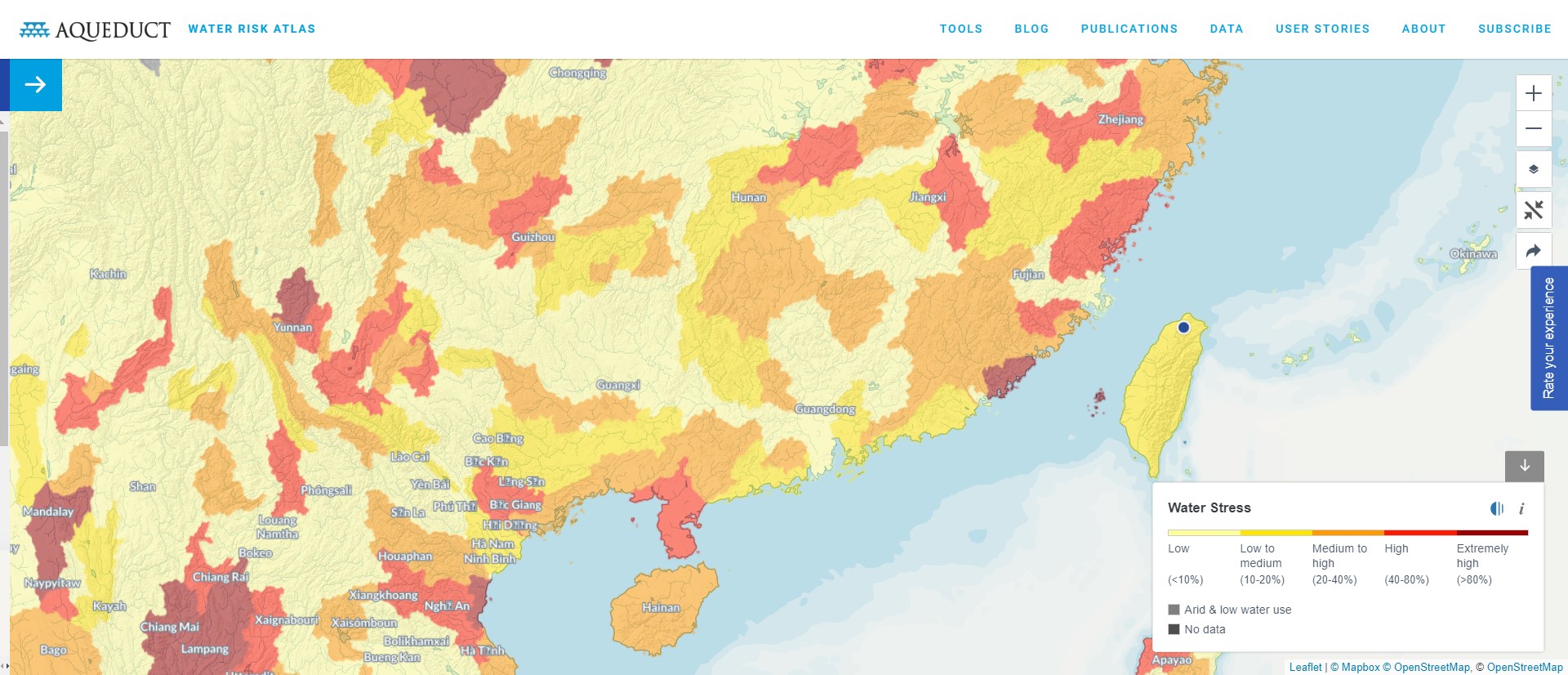

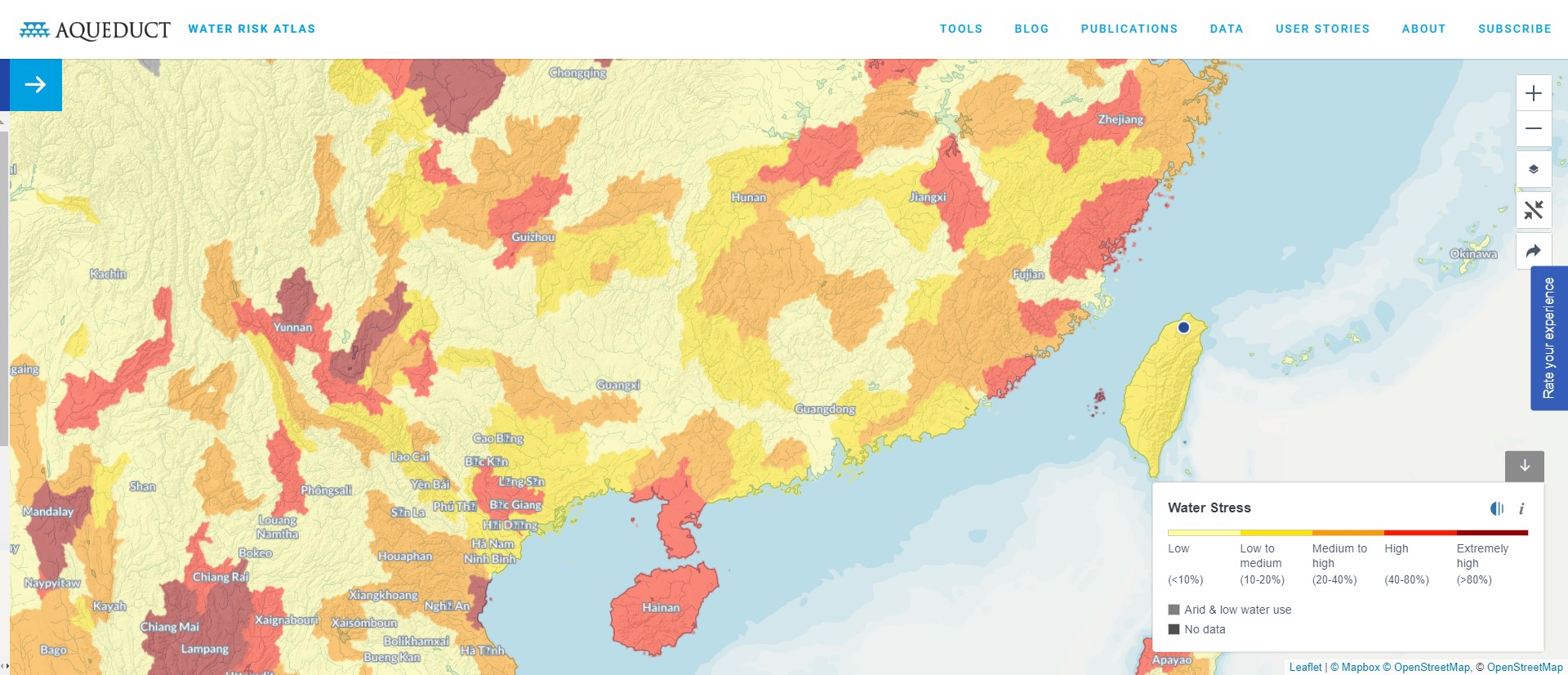

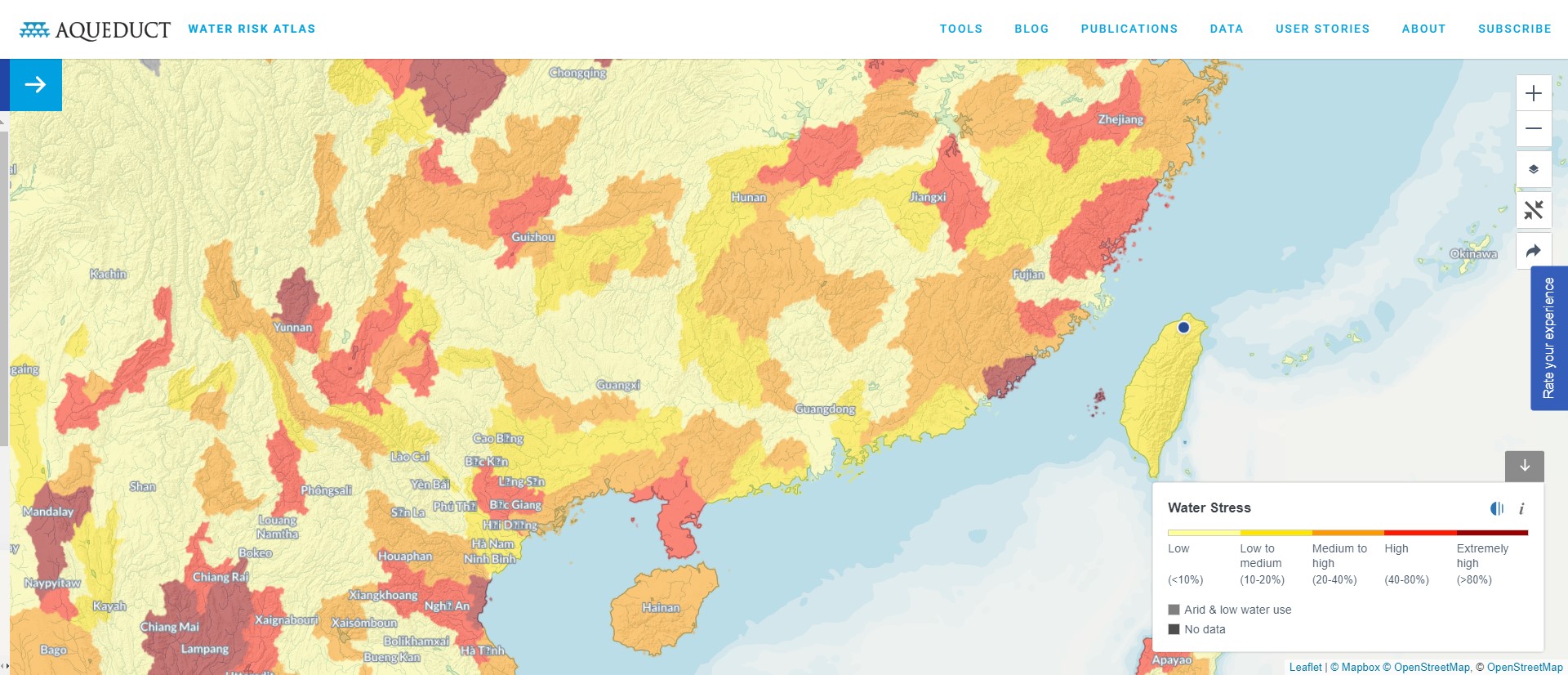

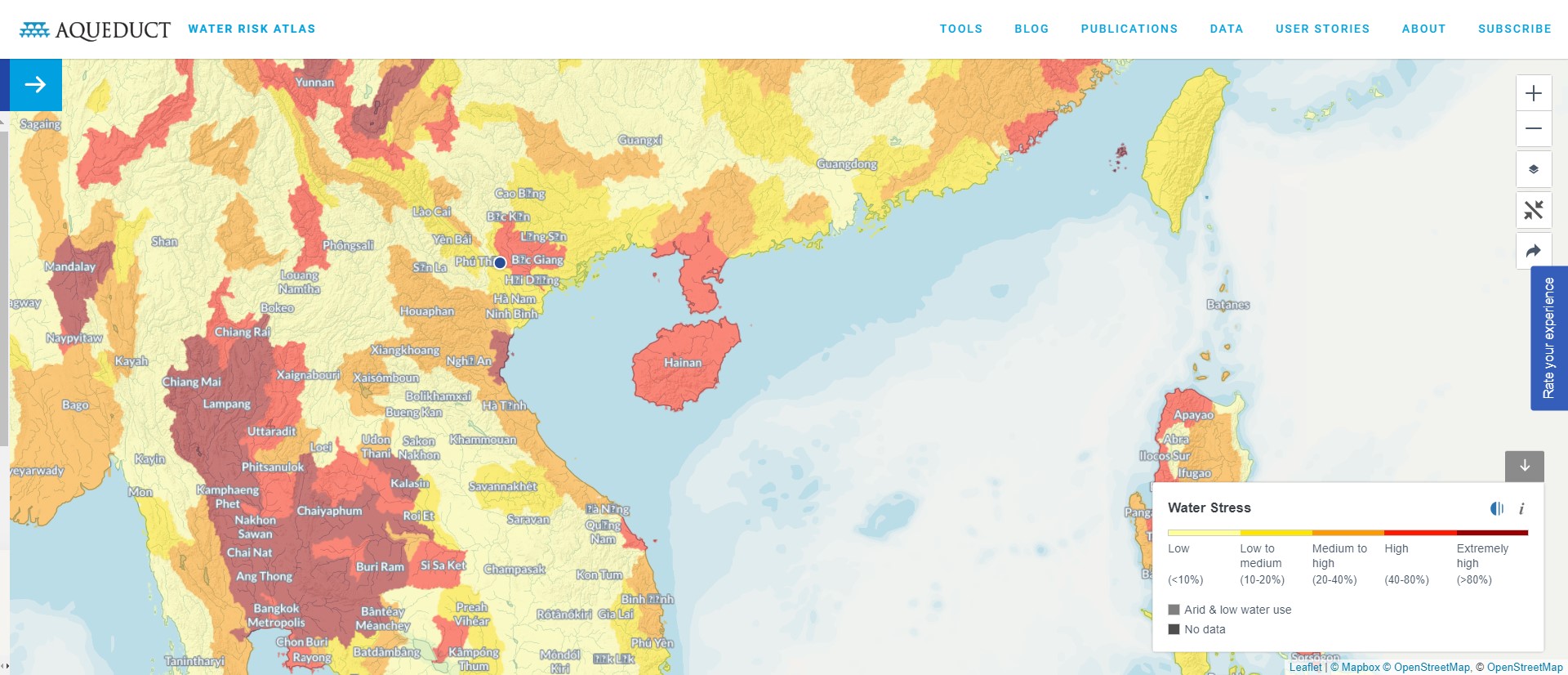

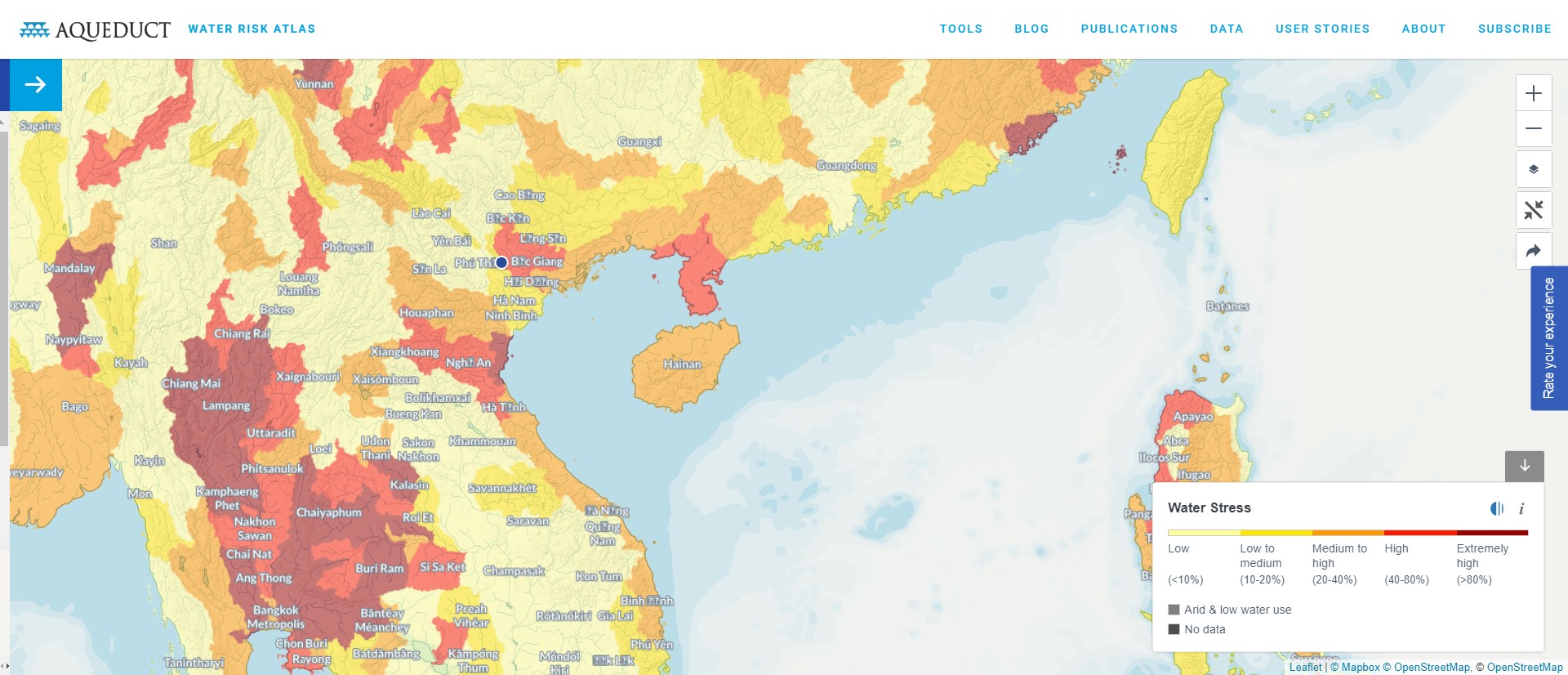

Pressure of Water Shortage

| Scenario Assumption | Factory Location | Base Year | Mid-term (2030) | Long-term (2050) |

|---|---|---|---|---|

| SSP1-2.6 Low-emission pathway | Taiwan |  Low-medium (10-20%) |  Low-medium (10-20%) |  Low-medium (10-20%) |

| SSP1-2.6 Low-emission pathway | Vietnam (Khai Quang Industrial Zone) |  Low-medium (10-20%) |  Low-medium (10-20%) |  Low-medium (10-20%) |

| SSP1-2.6 Low-emission pathway | Vietnam (Bai-Shan II Industrial Park) |  Medium-high (20-40%) |  Medium-high (20-40%) |  Medium-high (20-40%) |

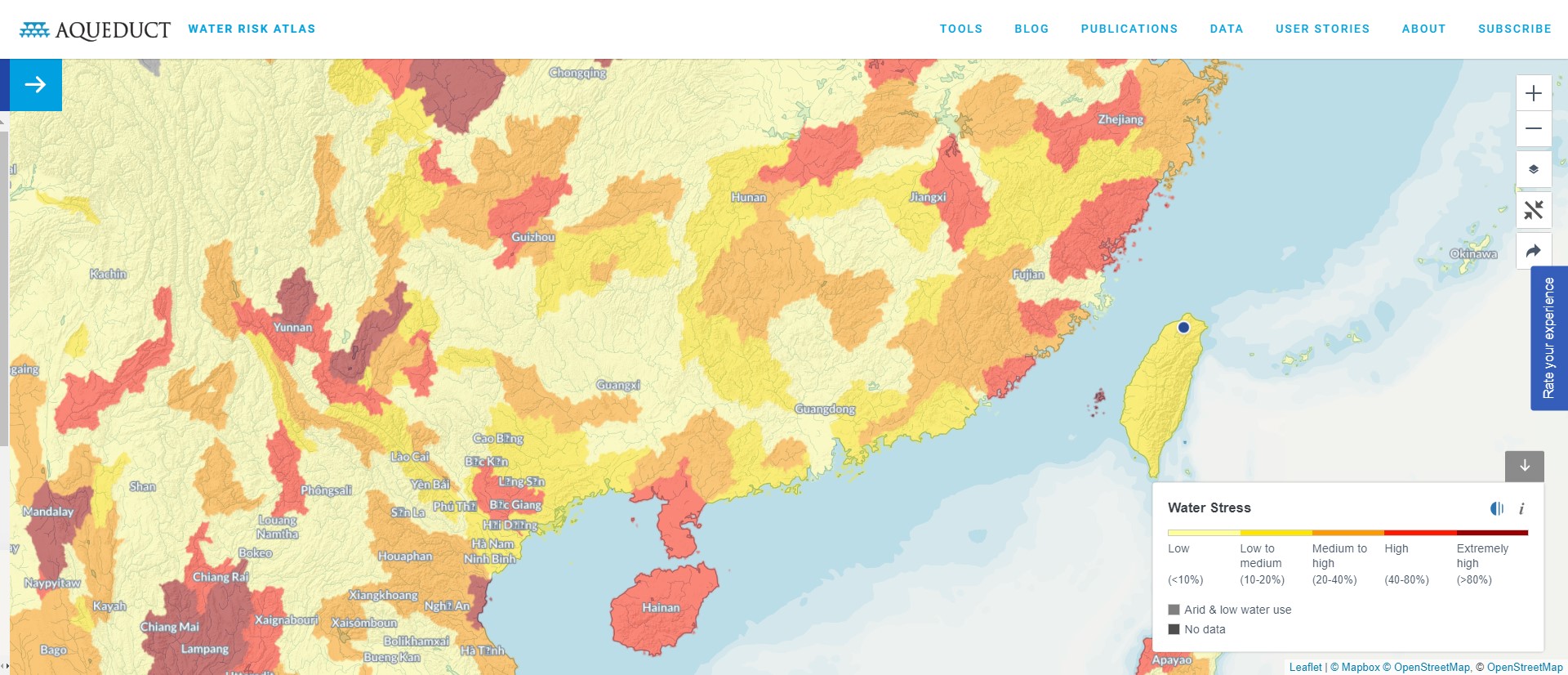

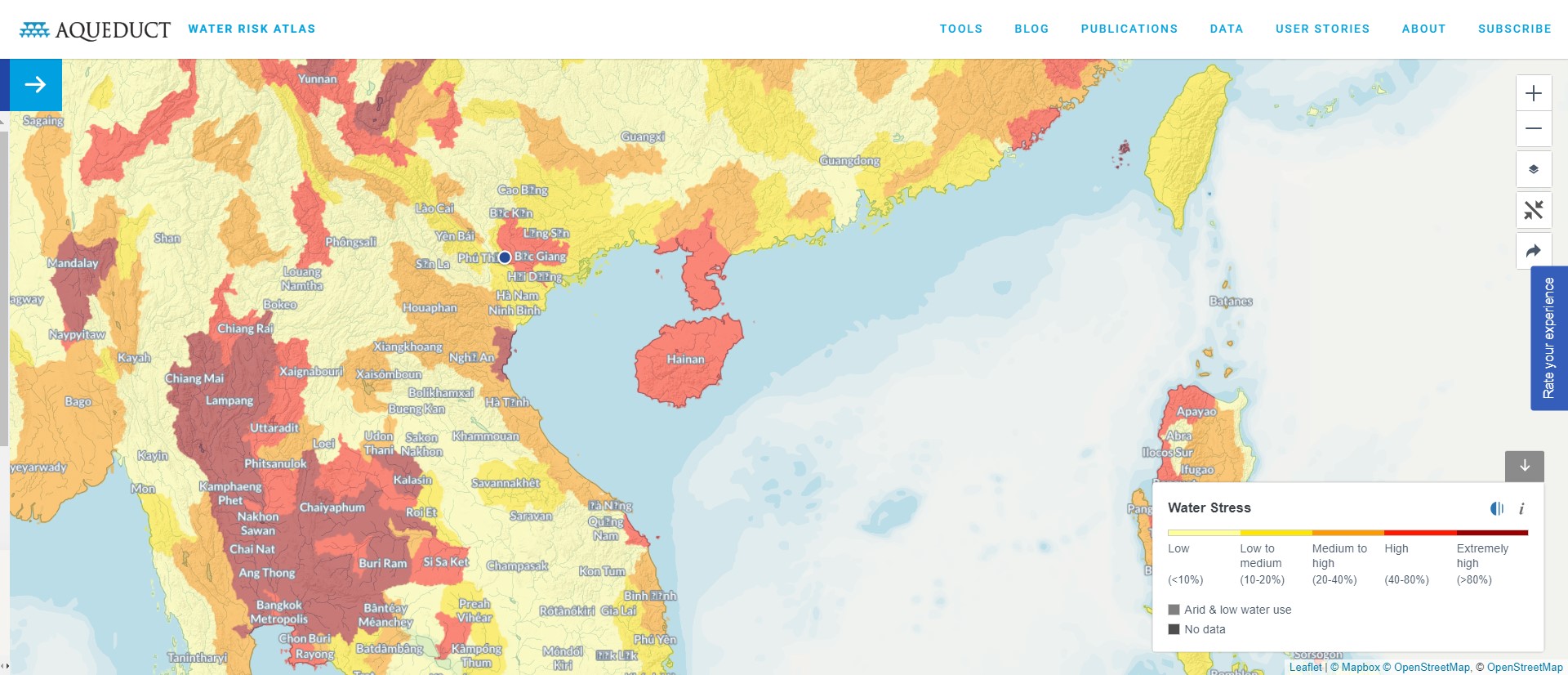

| Scenario Assumption | Factory Location | Base Year | Mid-term (2030) | Long-term (2050) |

|---|---|---|---|---|

| SSP5-8.5 High-emission pathway | Taiwan |  Low-medium (10-20%) |  Low-medium (10-20%) |  Low-medium (10-20%) |

| SSP5-8.5 High-emission pathway | Vietnam (Khai Quang Industrial Zone) |  Low-medium (10-20%) |  Low-medium (10-20%) |  Low-medium (10-20%) |

| SSP5-8.5 High-emission pathway | Vietnam (Bai-Shan II Industrial Park) |  Medium-high (20-40%) |  High (40-80%) |  High (40-80%) |

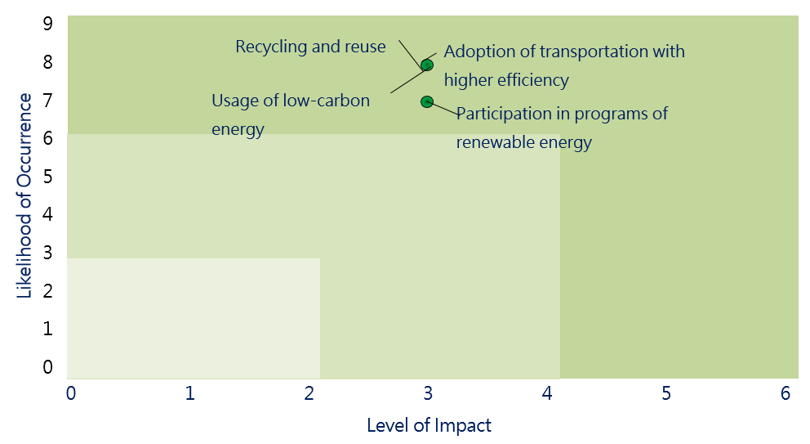

Impacts on Strategies, Operations, and Financial Planning Resulting from Climate Change Opportunities

| Types | Climate-related Risks and Opportunities | Characteristic Description of the Impact on Eurocharm | Scope of Influence | Severity | Time of Occurrence | Scenario Description of the Financial Impact to Eurocharm |

|---|---|---|---|---|---|---|

| Resource Efficiency | Adoption of more efficient transportation | International brand automakers are actively promoting the electric vehicle market and participation in the electric vehicle team. | The Company’s direct operation | Minor | Mid-term | ● In August 2023, fuel-powered business vehicles were replaced with a Vinfast electric car, costing about NT$1,747 thousand (VDN 1,336 million). Calculated by the accumulated mileage of 2,511 kilometers in September 2023, this change is estimated to save 6,883,727 Vietnamese Dong per month and reduce emissions by 0.35 tons of CO2e. |

| Resource Efficiency | Recycling and reuse | In response to the demand of international brand automakers, our company has reduced the amount of waste and is using recycled materials (waste aluminum). | The Company’s direct operation | Minor | Mid-term | ● In 2023, the aluminum scrap generated during the production process was directly recycled through aluminum furnaces. The amount to be reused was 81 tons, accounting for 2.17% of the total. |

| Water Resource Efficiency | Recycling wastewater | In response to the demand of international brand automakers, our company is implementing a water management plan that enhances recycling of the wastewater generated during the production process. | The Company’s direct operation | Minor | Mid-term | ● In 2023, the wastewater recycling rate at VPIC1 in Vietnam exceeded 12.53%, with a total of 26,705 tons of water having been recycled. |

| Energy Resources | The use of low carbon energy | In response to the demand of international brand automakers, our company have reduced energy usage while adopting renewable resources. On February 4, 2023, the Ministry of Industry and Trade of Vietnam issued the “Action Plan for Climate Change and Green Growth.” The action plan sets targets for 2030 and outlooks for 2050, including achieving a 15-20% share of renewable energy in the primary energy supply by 2030, reaching 25-30% by 2045, and limiting greenhouse gas emissions from the power sector to approximately 42 million tons CO2e by 2050. In order to achieve the nationally determined contribution (NDC) goals, our company needs to invest in building renewable energy facilities and replacing old equipment. | Upstream or our suppliers The Company’s direct operation Downstream or our customers | Minor | Mid-term | ● The Vietnamese electricity market has not been liberalized, and Vietnam Electricity Group (EVN) does not purchase renewable energy from businesses. ● Since June 2023, our company has been evaluating options, such as self-installation of solar equipment or renting rooftops to purchase green electricity for self-use, to replace a portion of the internal electricity usage, reducing the cost of purchasing electricity. In addition, the design of our Plant Six has already included installation of solar panels. |

Our Management Process of Climate-related Risks

To address climate change risks and based on the risk scenario analysis, the Group has developed response plans, served as a reference for formulating strategies facing physical climate risks. Additionally, in response to phenomena resulted from climate change, including sea-level rise caused by increasing average temperatures, sea-level rise and flooding caused by increased rainfall, and droughts caused by extreme weather, the Group has devised various plans to mitigate and adapt to climate-related risks. Furthermore, water inventory and water storage days are used as key indicators to increase process water recycling rates.

How Identification, Evaluation, and Management Process of Climate-related Risks Integrate with the Organization’s overall Risk Management System

The Group established a Risk Committee in June 2022, conducting annual risk identification and assessment, implementing preventive measures for high-risk projects, and conducting regular monitoring.

The Goals and Indicators

Disclose the metrics used by the organization to assess climate related risks and opportunities in line with its strategy and risk management process

Indicators used to assess climate-related risks and opportunities in accordance with the strategy and risk management process. The Group is concerned about the impact of climate issues on its operation. Therefore, the general manager reports to the board of directors on the commitment and concern for relevant goals, focusing on the following matters:

Disclosure of Greenhouse Gas Emission of Scope 1, 2 and 3 (if applicable) and Their Relevant Risks

Greenhouse Gas Emission

Every June and December are the Group’s environmental protection promotion months, aiming to educate employees on various energy-saving and carbon reduction policies. The Group also sets annual energy-saving targets to manage each production base, tracks emission reduction achievements, and publicly discloses them on the Company’s website. The Group conducts ISO 14064-1 greenhouse gas inventory and commissions SGS and BSI for third-party assurance. Due to changes in operational activities following the lift of pandemic restrictions, the baseline year has been adjusted. Details follow the Greenhouse Gas Management webpage.

Relevant Risks

The Company has included greenhouse gas emissions as one of the energy-saving and carbon-reduction performance indicators, reporting quarterly to the Sustainability Management Committee. The EU Carbon Border Adjustment Mechanism (CBAM) came into effect on May 17, 2023, with a transition period for its implementation from October 1, 2023, to December 31, 2025. In June 2022, the U.S. Senate introduced the Clean Competition Act (CCA) draft, which has not yet been formally passed. If enacted, the U.S. will begin levying a carbon tax in 2024, covering locally produced goods and products imported from other countries. Taiwan’s Climate Act has been passed, with the current carbon fee collection targeting manufacturing and electricity industries with annual emissions exceeding 25,000 metric tons, expected to commence in 2025. Currently, the emission from Eurocharm TW does not exceed the 25,000 metric ton threshold, thus it is not affected by carbon fee collection in Taiwan, but the possibility of future reductions in the threshold is being closely monitored.

Goals set by the organization for managing climate-related risks and opportunities and its performance of realizing the goals

To effectively manage the impact of climate change-related risks and opportunities on the Group, we have completed the greenhouse gas inventory and third-party verification in 2022. In August and December 2023, we have completed the introduction of ISO 50001 energy management system and its third-party verification at our operation sites in Vietnam and Taiwan. From September to December 2023, VPIC1 in Vietnam implemented ISO 14067 Product Carbon Footprint, continuously improving the setting of climate change goals and indicators to enhance corporate resilience as well as drive industry innovation.

| Short-term Goals (2023) | Achievements in 2023 | Mid-term Goals (2024 to 2030) | Long-term Goals (2031 to 2050) |

|---|---|---|---|

| ● Eurocharm TW and Vietnam VPIC1 have introduced ISO 50001 Energy Management System. ● VPIC1 in Vietnam has implemented ISO 14067 Product Carbon Footprint ● Overall emission reduction decreases by 1% for each subsidiary. ● Annual energy-saving is targeted at least 1% at Eurocharm TW and Vietnam VPIC1. | ● In August and December 2023, we have completed the introduction of ISO 50001 energy management system and its third-party verification at our operation sites in Vietnam and Taiwan. Every year, improvement plans of energy saving are proposed, gradually replacing our equipment to highly efficient ones and reforming the production process. ● From September to December 2023, VPIC1 in Vietnam implemented ISO 14067 Product Carbon Footprint. | ● Emission from Vietnam VPIC1 to be reduced by 3% annually, and emission from Eurocharm TW to be reduced by 2% annually. ● Annual energy-saving target exceeds 7% for Eurocharm TW and Vietnam VPIC1. ● Installation or purchase of solar facility (e.g. green/blue hydrogen power generation); renewable energy accounts for 20%. ● Introduction of AIOT smart management (MES, AOI smart production, EMS system, etc.) ● Increase the usage of recycled aluminum. ● Increase the recycling and reuse of the wastewater from painting production line. ● Introduction of liquid painting; improvement of die casting techniques | ● Emission from Vietnam VPIC1 to be reduced by 5% annually, and emission from Eurocharm TW to be reduced by 3% annually. ● Annual energy-saving target exceeds 3% for Eurocharm TW and Vietnam VPIC1. ● Installation or purchase of solar facility (e.g. green/blue hydrogen power generation); renewable energy accounts for 50%. ● Enhance the usage of recycled aluminum. ● Enhance the recycling and reuse of the wastewater from painting production line. ● Introduction of liquid painting; improvement of die casting techniques ● To adopt and use low carbon materials. ● To purchase land for agrivoltaics energy; plant trees for application of forest carbon sink. |